Buying a sports car is exciting, but insurance costs can significantly affect your budget. Some sports cars cost only slightly more to insure than regular vehicles, while others can double your annual premium. This guide explains how much sports car insurance typically costs, what factors influence rates, and practical ways to save money. You'll also learn how choosing the right used sports car can help reduce both purchase and insurance expenses.

What Is Sports Car Insurance?

Before comparing insurance prices, it is important to understand what sports car insurance actually means. Many buyers assume sports cars require a completely different type of insurance policy, but that is not exactly how it works.

Insurance companies generally use the same basic coverage types for sports cars and regular vehicles. The difference is that sports cars are often viewed as higher-risk vehicles because of their performance capabilities, repair costs, and claim history.

For budget-conscious buyers, understanding how insurers evaluate sports cars can help avoid unexpected expenses. A used Mazda MX-5 Miata may cost far less to insure than a Porsche 911, even though both are considered sports cars. Knowing these differences before buying can save thousands of dollars over the life of the vehicle.

Is There a Separate Insurance Policy for Sports Cars?

In most cases, there is no special insurance policy called "sports car insurance."

Sports car owners purchase the same types of coverage available to other drivers, including:

- Liability insurance

- Collision coverage

- Comprehensive coverage

- Uninsured motorist coverage

- Medical payments coverage

- Personal injury protection (where required)

The difference is that insurance companies calculate premiums differently when a vehicle is classified as a sports car.

For example, a driver insuring a Toyota Camry and another driver insuring a Toyota GR86 may receive different quotes even if they have identical driving records. The insurer views the GR86 as a higher-performance vehicle and may assign a higher risk level.

Some high-value performance vehicles may require specialized coverage options, particularly for:

- Collector cars

- Exotic vehicles

- Limited-production sports cars

- Modified performance cars

However, for most drivers shopping for vehicles such as a Ford Mustang, Chevrolet Camaro, Subaru BRZ, or Mazda MX-5 Miata, standard auto insurance policies are typically sufficient.

How Sports Car Insurance Differs From Standard Auto Insurance

The main difference between sports car insurance and insurance for a regular vehicle is cost.

Insurance companies examine large amounts of data when determining premiums. If a particular type of vehicle generates more claims, more severe accidents, or higher repair bills, insurers usually charge more to cover that risk.

Sports cars often receive higher premiums because they are associated with:

- Faster acceleration

- Higher top speeds

- More expensive repairs

- Costlier replacement parts

- Increased theft risk

- Larger claim payouts

For example, replacing a damaged bumper on a family sedan may cost significantly less than repairing body panels on a luxury sports car.

Performance vehicles also tend to attract drivers who use the vehicle differently than the average commuter. Even if an individual owner drives responsibly, insurers price policies based on overall risk patterns across thousands of drivers.

That said, not every sports car is expensive to insure.

A used Subaru BRZ or Mazda MX-5 Miata may have insurance rates that are surprisingly reasonable compared to some luxury SUVs or large pickup trucks.

This is why buyers should always compare quotes before assuming a vehicle is unaffordable to insure.

Who Typically Buys Sports Car Insurance?

Sports car insurance is purchased by a wide range of drivers, not just racing enthusiasts or luxury car owners.

Common buyers include:

- Young professionals

- Driving enthusiasts

- Weekend hobby drivers

- Retirees

- First-time sports car owners

- Collectors

- Budget-conscious buyers seeking affordable performance

For example, a 24-year-old buyer may purchase a used Ford Mustang EcoBoost because it offers sporty styling and strong performance without the cost of a high-end luxury vehicle.

Another buyer may choose a used Toyota GR86 from an auto auction because it provides an engaging driving experience while remaining relatively affordable to own.

Some sports car owners use their vehicles every day for commuting, while others drive them only on weekends or for special occasions.

Insurance companies consider these usage patterns when determining premiums. A vehicle driven 5,000 miles per year may cost less to insure than the same model driven 20,000 miles annually.

What Do Insurance Companies Consider a Sports Car?

Many drivers assume that a sports car is simply a vehicle that looks fast or has two doors. Insurance companies see things differently. When insurers classify a vehicle, they focus on risk rather than appearance.

A car's insurance category is usually based on factors such as horsepower, acceleration, repair costs, theft rates, historical claims data, and vehicle value. This is why two vehicles that look similar can have very different insurance premiums.

Understanding what insurers consider a sports car can help buyers avoid surprises when requesting quotes. In some cases, a vehicle that appears practical may be classified as a sports car, while a flashy-looking vehicle may have relatively affordable insurance rates.

Common Characteristics of Sports Cars

Although every insurance company uses its own rating system, most sports cars share several common characteristics.

Typical features include:

- Strong acceleration

- Above-average horsepower

- Sport-tuned suspension

- Performance-oriented handling

- Lightweight construction

- Lower ride height

- Rear-wheel-drive or performance all-wheel-drive systems

- Two-door or coupe body styles

Examples include:

- Mazda MX-5 Miata

- Toyota GR86

- Subaru BRZ

- Nissan Z

- Porsche 911

These vehicles are designed with driving performance as a major priority.

However, appearance alone does not determine classification.

For example, a modern sports sedan may have four doors and a spacious interior but still receive sports car insurance rates because of its performance capabilities.

Insurance companies focus more on how a vehicle performs and how expensive it is to insure than on how it looks.

Performance Features That Affect Insurance Rates

Performance is one of the biggest factors affecting insurance premiums.

The more capable a vehicle is in terms of speed and acceleration, the more likely it is to be classified as a sports car.

Features that often increase insurance costs include:

- High horsepower ratings

- Turbocharged engines

- Supercharged engines

- High-performance braking systems

- Advanced performance packages

- Track-oriented equipment

- Performance tires

For example, a 300-horsepower vehicle will generally be viewed as a greater risk than a similar model producing 180 horsepower.

Insurance companies often associate higher performance with:

- More aggressive driving behavior

- Higher accident severity

- Greater repair expenses

- Increased claim payouts

Acceleration can also play a major role.

A vehicle capable of reaching 60 mph in five seconds may receive higher insurance rates than a vehicle requiring eight seconds, even if both have similar purchase prices.

This does not mean every performance vehicle is expensive to insure, but strong performance characteristics usually contribute to higher premiums.

Sports Cars vs. Muscle Cars vs. Performance Sedans

Many buyers are surprised to learn that insurance companies do not always separate sports cars, muscle cars, and performance sedans into completely different categories.

All three may receive elevated insurance rates because they share similar risk factors.

Sports Cars

Sports cars typically prioritize handling, agility, and driver engagement.

Examples include:

- Mazda MX-5 Miata

- Toyota GR86

- Subaru BRZ

- Porsche 911

- Nissan Z

These vehicles are often smaller, lighter, and designed primarily for performance.

Muscle Cars

Muscle cars traditionally focus on straight-line speed and powerful engines.

Examples include:

- Ford Mustang GT

- Chevrolet Camaro SS

- Dodge Challenger R/T

- Dodge Challenger Scat Pack

Muscle cars frequently have large engines and high horsepower ratings, which can lead to higher insurance premiums.

Performance Sedans

Performance sedans combine practicality with strong performance.

Examples include:

- BMW M3

- Mercedes-AMG C63

- Cadillac CT4-V Blackwing

- Audi RS5 Sportback

Although these vehicles offer four doors and family-friendly features, insurers often view them similarly to sports cars because of their performance capabilities.

From an insurance perspective, all three categories can generate higher premiums if they present increased accident risk or repair costs.

Why Some Cars Are Classified as Sports Cars Even if They Do Not Look Like One

One of the most confusing aspects of sports car insurance is that some vehicles receive sports car classifications despite looking like ordinary sedans or hatchbacks.

This happens because insurance companies rely on data rather than styling.

For example, a vehicle may appear practical but still have:

- A powerful turbocharged engine

- High-performance suspension

- Sport-tuned handling

- Rapid acceleration

- Expensive replacement parts

Vehicles such as:

- Volkswagen Golf R

- Honda Civic Type R

- Hyundai Elantra N

- Tesla Model 3 Performance

may not resemble traditional sports cars, yet they often receive higher insurance rates because of their performance characteristics.

Similarly, some luxury SUVs can cost more to insure than certain sports cars because they are expensive to repair and replace.

This is why buyers should never assume insurance costs based solely on appearance.

A Toyota GR86 may actually cost less to insure than a luxury performance sedan worth twice as much.

Why Is Insurance More Expensive for Sports Cars?

Many buyers are surprised when they request insurance quotes for a sports car and discover that the premium is significantly higher than for a regular sedan or crossover. Even if two vehicles have similar market values, the sports car often costs more to insure.

Insurance companies determine rates by analyzing risk. If a vehicle is more likely to be involved in accidents, stolen, or generate expensive claims, insurers typically charge higher premiums to offset those risks.

Sports cars are often associated with several factors that increase claim costs. Understanding these factors can help buyers make smarter purchasing decisions and avoid unexpected ownership expenses.

Higher Accident Risk

One of the main reasons sports cars cost more to insure is their higher accident risk.

Insurance companies study millions of claims and use historical data to identify patterns. Vehicles that are involved in accidents more frequently often receive higher insurance rates.

Sports cars are commonly associated with:

- Faster driving

- Aggressive acceleration

- Higher-speed travel

- Enthusiast driving behavior

Even though many owners drive responsibly, insurance companies base premiums on overall statistics rather than individual intentions.

For example, a 35-year-old driver may carefully use a Chevrolet Camaro only for commuting, but the insurer evaluates the vehicle based on how Camaro drivers as a group perform in accident data.

Higher accident frequency means:

- More insurance claims

- More repair costs

- Greater financial risk for insurers

As a result, premiums often increase.

Faster Acceleration and Top Speeds

Performance capabilities play a major role in sports car insurance pricing.

Many sports cars are designed to accelerate quickly and achieve higher top speeds than regular passenger vehicles.

Examples include:

- Ford Mustang GT

- Nissan Z

- Chevrolet Corvette

- Porsche 911

- Mercedes-AMG GT

From an insurance perspective, faster acceleration can increase risk because it may contribute to:

- Loss-of-control accidents

- High-speed collisions

- More severe crash damage

For example, a Toyota Camry and a Ford Mustang GT may have similar purchase prices, but the Mustang's performance capabilities often result in higher insurance premiums.

Insurance companies are not necessarily charging for speed itself. Instead, they are pricing the increased likelihood and potential severity of claims associated with high-performance vehicles.

This is one reason why vehicles with powerful engines and rapid acceleration often cost more to insure than economy cars.

More Expensive Repairs and Parts

Repair costs are another major factor.

Sports cars often use specialized components that cost more to repair or replace after an accident.

Examples include:

- Performance brakes

- Specialized suspension systems

- High-performance tires

- Aluminum body panels

- Carbon-fiber components

- Premium lighting systems

Even relatively minor accidents can generate expensive repair bills.

For example, replacing a damaged bumper on a family sedan may cost considerably less than repairing the front-end components of a luxury sports car.

Performance tires alone can cost several times more than standard tires found on economy vehicles.

Luxury sports cars such as:

- Porsche 911

- Jaguar F-Type

- Mercedes-AMG GT

typically have particularly high repair costs because of expensive parts and specialized labor requirements.

Higher repair costs lead directly to higher insurance premiums.

Increased Theft Rates

Sports cars are often attractive targets for thieves.

Their popularity, performance parts, and resale value can make them more vulnerable to theft than many ordinary vehicles.

Insurance companies closely track:

- Vehicle theft frequency

- Recovery rates

- Claim payouts

Some sports cars are stolen because:

- They have valuable components.

- They are desirable on the used-parts market.

- They attract strong demand among thieves.

For example, performance wheels, engines, body panels, and electronic systems can be valuable when sold separately.

If a vehicle model has a history of frequent theft claims, insurers may increase premiums even if the owner has never experienced a theft-related incident.

This additional risk is reflected in comprehensive coverage rates, which protect against theft and related losses.

Higher Claim Severity

Insurance companies focus not only on how often claims occur but also on how expensive those claims become.

This concept is known as claim severity.

Sports car claims are often more costly because accidents involving performance vehicles can result in:

- Greater vehicle damage

- Higher repair bills

- Increased medical expenses

- Larger liability claims

For example, a low-speed parking lot accident involving a compact sedan may result in a relatively small insurance payout.

A similar accident involving a luxury sports car with advanced sensors, premium paint, and specialized body panels may cost several times more to repair.

The higher the average claim payout for a particular model, the more likely insurers are to charge elevated premiums.

This explains why some expensive sports cars can have dramatically higher insurance costs than vehicles with similar purchase prices.

Greater Likelihood of Aggressive Driving

Insurance companies also consider driver behavior patterns associated with certain vehicles.

Sports cars tend to attract buyers who value:

- Performance

- Acceleration

- Handling

- Driving excitement

While most owners drive responsibly, insurers use historical data to evaluate how drivers of specific models behave overall.

Some sports cars have a higher incidence of:

- Speeding violations

- Reckless driving citations

- Performance-related accidents

- High-risk driving behavior

For example, a young driver purchasing a Dodge Challenger Scat Pack may face substantially higher insurance rates than someone driving a midsize sedan with the same driving record.

This does not mean every sports car owner drives aggressively. However, insurance pricing reflects statistical trends observed across thousands of policyholders.

The stronger the correlation between a vehicle model and risky driving behavior, the higher the insurance premiums are likely to be.

How Much Does Sports Car Insurance Cost?

One of the biggest questions buyers ask before purchasing a sports car is how much insurance will actually cost. Unfortunately, there is no single answer. Insurance premiums can vary dramatically depending on the vehicle, driver profile, location, coverage limits, and insurer.

A Mazda MX-5 Miata may cost only slightly more to insure than a family sedan, while a Porsche 911 or Mercedes-AMG GT can cost several times more. This is why insurance should always be considered before purchasing a performance vehicle.

For budget-conscious buyers, understanding the typical cost ranges can help avoid buying a sports car that becomes too expensive to own. Insurance is often one of the largest ongoing expenses associated with a performance vehicle.

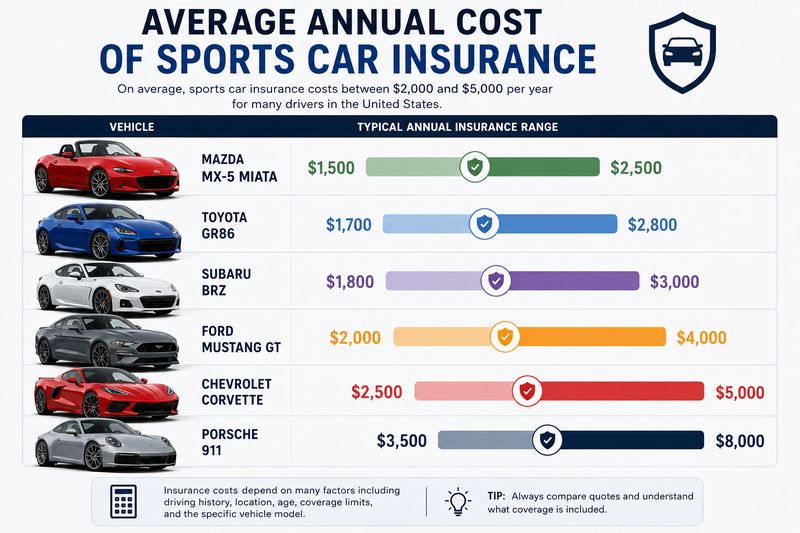

Average Annual Cost of Sports Car Insurance

On average, sports car insurance costs between $2,000 and $5,000 per year for many drivers in the United States.

However, actual premiums can vary significantly.

Examples of typical annual insurance ranges include:

- Mazda MX-5 Miata: approximately $1,500–$2,500

- Toyota GR86: approximately $1,700–$2,800

- Subaru BRZ: approximately $1,800–$3,000

- Ford Mustang GT: approximately $2,000–$4,000

- Chevrolet Corvette: approximately $2,500–$5,000

- Porsche 911: approximately $3,500–$8,000+

These figures are only examples and can vary based on:

- Driver age

- Driving history

- ZIP code

- Coverage levels

- Insurance company

For example, a 40-year-old driver with a clean record may pay thousands less per year than a 20-year-old driver insuring the exact same vehicle.

The difference can be substantial enough to change which sports car makes financial sense to purchase.

Average Monthly Cost of Sports Car Insurance

Most drivers think about insurance in monthly terms because it affects their ongoing budget.

Sports car insurance commonly ranges from approximately:

- $125 to $450 per month

For some high-performance vehicles, monthly premiums may exceed:

- $500

- $700

- or even $1,000

for high-risk drivers.

Consider these examples:

- Mazda MX-5 Miata: roughly $125–$210 per month

- Toyota GR86: roughly $140–$230 per month

- Ford Mustang GT: roughly $170–$330 per month

- Chevrolet Corvette: roughly $210–$420 per month

- Porsche 911: roughly $300–$700+ per month

A buyer shopping for a sports car with a monthly budget of $600 should remember that insurance may consume a significant portion of that amount.

For example, purchasing a used Mustang for $350 per month may seem affordable until a $250 monthly insurance bill is added.

Looking at the total monthly ownership cost is often more important than focusing on the vehicle payment alone.

Cost Comparison With Regular Vehicles

Sports cars typically cost more to insure than regular passenger vehicles.

For comparison, many family sedans and compact cars may cost:

- $1,200–$2,000 annually

- $100–$170 monthly

to insure.

Consider a simple example:

Toyota Camry

- Annual insurance: approximately $1,500

- Monthly insurance: approximately $125

Toyota GR86

- Annual insurance: approximately $2,300

- Monthly insurance: approximately $190

The difference may seem manageable.

However, compare a family sedan with a higher-performance vehicle:

Honda Accord

- Annual insurance: approximately $1,600

Chevrolet Corvette

- Annual insurance: approximately $4,000

The gap becomes much larger.

Sports cars generally generate higher premiums because insurers expect:

- Higher repair costs

- Greater accident severity

- Increased theft risk

- More expensive claims

That does not mean every sports car is expensive.

In some cases, an older used sports car may cost less to insure than a newer luxury SUV worth twice as much.

This is why obtaining insurance quotes before purchasing a vehicle is essential.

Insurance Costs by Driver Age Group

Driver age is one of the biggest factors influencing sports car insurance premiums.

Insurance companies view younger drivers as statistically riskier because they have less driving experience and generate more claims on average.

Drivers Under 25

This group often pays the highest premiums.

For example, a 21-year-old insuring a Ford Mustang GT may receive quotes that are two or three times higher than those offered to an older driver.

Many young drivers see annual premiums ranging from:

- $3,000 to $8,000+

depending on the vehicle.

Drivers Ages 25–40

Premiums often decrease significantly after age 25, assuming the driver maintains a clean record.

Many sports car owners in this group receive more competitive rates because they have:

- More driving experience

- Lower claim frequency

- Better insurance histories

Drivers Ages 40–65

This age group often receives some of the lowest sports car insurance rates.

Many insurers consider these drivers relatively low risk, particularly if they have:

- Clean driving records

- Stable insurance histories

- Low annual mileage

Senior Drivers

Rates may remain competitive for many older drivers, although premiums sometimes increase again as insurers adjust for age-related risk factors.

For example, a retired driver who only uses a sports car for weekend trips may qualify for lower premiums because of limited annual mileage.

This demonstrates how insurance pricing depends on far more than the vehicle itself.

Compare Sports Cars Before You Place a Bid

Insurance costs can vary by thousands of dollars depending on the vehicle you choose. Before buying a sports car, browse auction inventory, review vehicle history reports, and compare models that offer the best balance of performance and affordability.

- ✅ 150,000+ vehicles available online

- ✅ Free vehicle history reports

- ✅ Affordable sports cars from U.S. auctions

- ✅ Bid on vehicles from home

Factors That Affect Sports Car Insurance Rates

Many buyers assume that sports car insurance is determined solely by the vehicle itself. In reality, insurance companies evaluate dozens of factors before calculating a premium. Two drivers can insure the same sports car and receive dramatically different quotes.

For example, a 45-year-old driver with a clean record may pay half as much as a 21-year-old driver insuring the same Ford Mustang. Likewise, a used Mazda MX-5 Miata in a low-crime area may cost significantly less to insure than a similar vehicle parked in a major city.

Understanding the factors that influence insurance rates can help buyers make smarter decisions and potentially save hundreds or even thousands of dollars each year.

Vehicle Make and Model

The specific vehicle you choose is one of the biggest factors affecting insurance costs.

Insurance companies maintain extensive databases showing:

- Accident frequency

- Theft rates

- Repair costs

- Claim severity

- Replacement expenses

for nearly every vehicle model on the road.

For example, a Mazda MX-5 Miata is often less expensive to insure than a Chevrolet Corvette because the Corvette generally produces larger claims and higher repair bills.

Similarly, a Toyota GR86 may cost less to insure than a Porsche 911 even though both are considered sports cars.

Insurance companies evaluate each model separately, which is why comparing quotes before purchasing a vehicle is so important.

Vehicle Value and Replacement Cost

More expensive vehicles usually cost more to insure.

If a vehicle is stolen or totaled, the insurance company may have to pay its market value. The higher that value, the greater the insurer's financial risk.

For example:

- A used Subaru BRZ worth $20,000 presents less replacement risk than

- A Porsche 911 worth $120,000.

Vehicle value also affects:

- Comprehensive coverage costs

- Collision coverage costs

- Total-loss claim payouts

Luxury sports cars often carry higher premiums because insurers may be responsible for much larger payouts following serious accidents or thefts.

This is one reason many budget-conscious buyers choose used sports cars rather than new ones.

Engine Size and Horsepower

Performance remains one of the defining characteristics of sports cars.

Vehicles with larger engines and higher horsepower ratings often receive higher insurance premiums because insurers associate them with greater risk.

Examples include:

- Faster acceleration

- Higher top speeds

- Increased accident severity

- Larger claim payouts

Consider two versions of the same vehicle:

- Ford Mustang EcoBoost

- Ford Mustang GT

The GT's larger engine and higher horsepower typically result in more expensive insurance.

Similarly, a Dodge Challenger Hellcat will generally cost much more to insure than a Dodge Challenger with a smaller engine.

While horsepower is not the only factor, it remains an important component of insurance pricing.

Driver Age and Experience

Driver age is one of the most influential factors in sports car insurance.

Insurance companies rely heavily on statistical data, and younger drivers generally produce more claims than experienced drivers.

Drivers under 25 often face the highest premiums because they are statistically more likely to be involved in accidents.

For example:

- A 22-year-old driver insuring a Chevrolet Camaro may pay significantly more than

- A 45-year-old driver with an identical vehicle and coverage package.

Experience matters as well.

Someone who has maintained continuous insurance coverage and a safe driving history for many years is usually viewed as a lower-risk customer.

As drivers gain experience and avoid accidents, premiums often decrease.

Driving Record and Claims History

Insurance companies closely examine your personal driving history.

Common factors include:

- Traffic violations

- Speeding tickets

- At-fault accidents

- Previous claims

- DUI convictions

- License suspensions

A driver with a clean record often receives much better rates than someone with multiple violations.

For example, two drivers may own identical Toyota GR86 models.

One has:

- No accidents

- No tickets

- Ten years of safe driving

The other has:

- Several speeding violations

- A recent at-fault accident

The second driver will likely pay substantially higher premiums.

Maintaining a clean driving record remains one of the most effective ways to reduce sports car insurance costs.

Location and ZIP Code

Where you live can significantly impact insurance rates.

Insurance companies evaluate risk based on geographic data such as:

- Accident frequency

- Vehicle theft rates

- Weather-related claims

- Population density

- Repair costs

A sports car insured in a large metropolitan area often costs more to insure than the same vehicle in a rural community.

For example, drivers in heavily populated cities may face higher premiums because insurers expect:

- More accidents

- More theft claims

- Greater traffic congestion

Even moving a few miles to a different ZIP code can sometimes affect insurance pricing.

This factor is largely outside the driver's control, but it plays a major role in premium calculations.

Annual Mileage

The more you drive, the more opportunities there are for accidents.

As a result, insurance companies often ask applicants to estimate their annual mileage.

Common mileage categories include:

- Under 5,000 miles

- 5,000–10,000 miles

- 10,000–15,000 miles

- More than 15,000 miles

A sports car driven only on weekends may cost less to insure than one used for a long daily commute.

For example:

- A retired owner who drives a Corvette 4,000 miles annually may receive a lower premium than

- A commuter driving the same vehicle 18,000 miles per year.

Lower mileage generally translates into lower risk.

Credit Score (Where Applicable)

In many states, insurance companies use credit-based insurance scores as part of their pricing models.

Research has shown that individuals with stronger credit histories often file fewer insurance claims.

As a result, insurers may offer lower premiums to applicants with higher credit scores.

Factors that may influence these scores include:

- Payment history

- Debt levels

- Credit utilization

- Length of credit history

For example, two drivers with identical vehicles and driving records may still receive different quotes because of differences in their credit profiles.

However, not all states allow insurers to use credit information when determining rates.

Local regulations vary, so the impact depends on where the policy is issued.

Coverage Limits and Deductibles

The amount of coverage you choose directly affects your insurance premium.

Policies with higher protection levels generally cost more.

Examples include:

- Higher liability limits

- Lower deductibles

- Expanded comprehensive coverage

- Additional endorsements

A deductible is the amount you pay before insurance coverage begins.

For example:

- A $500 deductible typically results in higher premiums.

- A $1,000 deductible often reduces premiums.

Many sports car owners lower their insurance costs by choosing higher deductibles, provided they can comfortably afford the out-of-pocket expense if a claim occurs.

The right balance depends on your financial situation and risk tolerance.

Sports Car Insurance Costs by Vehicle Category

Not all sports cars are equally expensive to insure. Some models are surprisingly affordable, while others can generate insurance bills that rival a monthly car payment.

Insurance companies evaluate each vehicle based on factors such as accident history, repair costs, theft rates, horsepower, and claim severity. As a result, two sports cars with similar performance may have very different insurance premiums.

For buyers on a budget, affordable sports cars often provide the best balance between driving enjoyment and manageable ownership costs. These vehicles deliver sporty handling and strong performance without the extreme insurance expenses associated with luxury or exotic models.

Affordable Sports Cars

Affordable sports cars are often the smartest choice for buyers who want a fun driving experience without facing overwhelming insurance costs.

Many of these vehicles offer:

- Good safety ratings

- Moderate horsepower

- Lower repair costs

- Strong reliability records

- Reasonable replacement values

Compared with high-end performance vehicles, they typically generate fewer costly insurance claims and are therefore less expensive to insure.

Popular budget-friendly sports cars include:

- Mazda MX-5 Miata

- Hyundai Veloster N

- Toyota GR86

- Subaru BRZ

While insurance rates vary by driver, these models are generally among the most affordable sports cars to insure in the United States.

Mazda MX-5 Miata Insurance Costs

The Mazda MX-5 Miata is frequently considered one of the cheapest sports cars to insure.

Several factors contribute to its relatively low insurance costs:

- Modest horsepower compared to many sports cars

- Strong safety reputation

- Lightweight design

- Lower purchase price

- Reasonable repair costs

Many drivers pay approximately:

- $1,500–$2,500 per year

- $125–$210 per month

for full coverage insurance.

The Miata is a good example of how a vehicle can provide a genuine sports car experience without generating extreme insurance expenses.

For a buyer comparing a used Miata with a larger V8-powered sports car, the insurance savings alone can amount to hundreds or even thousands of dollars per year.

This makes the Miata particularly attractive for budget-conscious enthusiasts.

Hyundai Veloster N Insurance Costs

The Hyundai Veloster N offers strong performance and sporty handling while often maintaining insurance costs below those of many traditional sports cars.

Although its turbocharged engine provides impressive performance, insurers typically view it differently than high-horsepower muscle cars or luxury sports cars.

Typical insurance costs often fall within:

- $1,700–$2,800 per year

- $140–$235 per month

depending on the driver's profile.

The Veloster N appeals to drivers who want:

- Practical daily transportation

- Sporty performance

- Modern technology

- Lower ownership costs

Because it combines hatchback practicality with performance features, it can be an appealing option for younger buyers seeking a balance between affordability and excitement.

However, younger drivers may still face higher premiums because insurers consider both the vehicle and the driver's age when determining rates.

Toyota GR86 Insurance Costs

The Toyota GR86 has become one of the most popular affordable sports cars on the market.

Its lightweight design and balanced performance make it appealing to enthusiasts, while its relatively modest purchase price helps keep insurance costs manageable.

Typical insurance premiums often range between:

- $1,700–$2,800 annually

- $140–$230 monthly

for many drivers.

The GR86 benefits from:

- Moderate horsepower

- Strong reliability reputation

- Lower replacement costs than luxury sports cars

- Widely available parts

For example, a driver comparing a Toyota GR86 with a Chevrolet Corvette may find that the GR86 costs thousands less per year to insure.

This can significantly reduce overall ownership expenses.

Many buyers shopping through auto auctions specifically target used GR86 models because they offer sports car styling and performance without the financial burden associated with more expensive vehicles.

Subaru BRZ Insurance Costs

The Subaru BRZ shares much of its engineering with the Toyota GR86, which means insurance costs are often similar.

Many drivers can expect to pay approximately:

- $1,800–$3,000 per year

- $150–$250 per month

for full coverage.

The BRZ remains one of the more affordable sports cars to insure because of its:

- Moderate engine output

- Reasonable vehicle value

- Strong safety equipment

- Relatively affordable repair costs

Insurance companies generally view the BRZ as a lower-risk performance vehicle than many high-horsepower muscle cars.

For example, a Subaru BRZ owner may pay substantially less than a driver insuring a Dodge Challenger Scat Pack or Ford Mustang GT.

This difference becomes especially important for younger buyers.

A first-time sports car owner often discovers that the BRZ provides an enjoyable driving experience while keeping insurance costs within a manageable budget.

For many drivers, the BRZ represents one of the best combinations of affordability, reliability, and performance available in the sports car market.

Mid-Range Sports Cars

Mid-range sports cars occupy the middle ground between affordable entry-level performance vehicles and high-end luxury sports cars. They typically offer more horsepower, faster acceleration, and stronger performance than vehicles such as the Mazda MX-5 Miata or Toyota GR86, but they remain significantly less expensive to purchase and insure than exotic models.

Popular vehicles in this category include:

- Ford Mustang

- Chevrolet Camaro

- Dodge Challenger

- Nissan Z

- Chevrolet Corvette

Insurance costs in this segment vary considerably because engine options, vehicle value, repair expenses, and driver demographics can differ greatly from one model to another.

For example, a Ford Mustang EcoBoost may be relatively affordable to insure, while a high-performance Corvette can cost substantially more despite both being considered sports cars.

Ford Mustang Insurance Costs

The Ford Mustang is one of the most recognizable sports cars in America and is available with several engine options that significantly affect insurance costs.

Typical insurance premiums often range between:

- $2,000–$4,000 per year

- $170–$330 per month

depending on:

- Driver age

- Driving history

- Coverage level

- Vehicle trim

The Mustang EcoBoost is usually the least expensive version to insure because it has:

- Lower horsepower than V8 models

- Lower purchase prices

- Reduced repair costs

Meanwhile, Mustang GT and high-performance variants generally command higher premiums because of:

- Larger engines

- Faster acceleration

- Higher claim severity

For example, a 35-year-old driver with a clean record may find a used Mustang EcoBoost surprisingly affordable to insure, while a younger driver purchasing a new Mustang GT may receive much higher quotes.

This is why many budget-conscious buyers view the EcoBoost as one of the most practical entry points into sports car ownership.

Chevrolet Camaro Insurance Costs

The Chevrolet Camaro is another popular performance vehicle that often carries moderate-to-high insurance costs.

Typical annual premiums commonly fall between:

- $2,100–$4,200

- $175–$350 per month

Insurance rates depend heavily on the engine configuration.

Camaro models equipped with:

- Four-cylinder engines

- V6 engines

are generally less expensive to insure than:

- SS models

- ZL1 performance variants

The Camaro's sporty image and strong performance capabilities contribute to higher insurance rates compared with many ordinary passenger vehicles.

However, compared to some luxury sports cars, insurance costs often remain relatively manageable.

Buyers shopping for a used Camaro can frequently reduce both purchase costs and insurance expenses by selecting older model years with lower replacement values.

Dodge Challenger Insurance Costs

The Dodge Challenger presents a unique case because it is available in an extremely wide range of performance levels.

Insurance premiums typically range from:

- $2,200–$4,500 per year

- $185–$375 per month

for many drivers.

Several factors influence Challenger insurance costs:

- Engine size

- Horsepower

- Theft rates

- Driver demographics

Base V6 models are generally much more affordable to insure than high-performance versions such as:

- R/T

- Scat Pack

- Hellcat

- Demon

The Challenger's popularity, powerful engine options, and relatively high theft rates can contribute to elevated insurance premiums.

For example, a Challenger Hellcat may cost thousands more per year to insure than a V6 Challenger, even when driven by the same person.

Budget-focused buyers often find that lower-trim Challenger models deliver the desired styling and comfort without the extreme insurance costs associated with high-horsepower versions.

Nissan Z Insurance Costs

The Nissan Z continues the legacy of Nissan's long-running line of sports cars and generally falls in the middle of the insurance-cost spectrum.

Many drivers pay approximately:

- $2,000–$3,800 annually

- $165–$320 monthly

for full coverage insurance.

Several factors help shape Nissan Z insurance costs:

- Sports car classification

- Strong performance capabilities

- Moderate production volumes

- Specialized parts

Although the Nissan Z offers impressive acceleration and performance, it typically remains less expensive to insure than many luxury sports cars.

For buyers who want a modern sports car experience without stepping into luxury pricing territory, the Nissan Z often represents a reasonable compromise.

A used Nissan Z purchased through an auto auction may also provide additional savings by lowering the vehicle's replacement value, which can help reduce insurance costs.

Chevrolet Corvette Insurance Costs

The Chevrolet Corvette is often considered one of the most affordable ways to access true high-performance sports car capabilities.

However, insurance companies still view the Corvette as a higher-risk vehicle than most cars in this category.

Typical premiums often range between:

- $2,500–$5,000 per year

- $210–$420 per month

depending on the driver's profile and vehicle generation.

Several factors contribute to higher Corvette insurance costs:

- Powerful engines

- Expensive body components

- Higher repair costs

- Larger claim payouts

Newer Corvette models often cost more to insure because:

- Replacement values are higher.

- Repair procedures are more complex.

- Parts are more expensive.

That said, older Corvettes can sometimes offer surprisingly affordable insurance rates because depreciation reduces replacement costs.

For example, a well-maintained used Corvette purchased at auction may cost significantly less to insure than a new luxury sports sedan with a similar market value.

Many enthusiasts consider the Corvette one of the best performance-per-dollar values available, but insurance should always be factored into the overall ownership budget.

Luxury and High-Performance Sports Cars

Luxury and high-performance sports cars sit at the top end of the insurance spectrum. These vehicles combine powerful engines, advanced technology, premium materials, and high replacement values, all of which contribute to higher insurance costs.

While they offer exceptional performance and prestige, they also present greater financial risk for insurance companies. Expensive repairs, specialized parts, and large claim payouts often result in significantly higher premiums than those associated with affordable or mid-range sports cars.

For buyers considering one of these vehicles, insurance costs should be included in the overall ownership budget before making a purchase decision.

Porsche 911 Insurance Costs

The Porsche 911 is one of the most iconic sports cars in the world and is often among the more expensive vehicles to insure.

Typical insurance costs frequently range between:

- $3,500–$8,000+ per year

- $300–$700+ per month

Several factors contribute to these higher premiums:

- High vehicle value

- Expensive replacement parts

- Specialized repair procedures

- Powerful performance capabilities

- Luxury-car claim history

Different Porsche 911 variants can also produce very different insurance costs.

For example:

- Carrera models typically cost less to insure than

- Turbo, GT3, or Turbo S models.

A used Porsche 911 may be less expensive to insure than a brand-new example because depreciation reduces the vehicle's replacement value.

However, maintenance and repair costs remain important considerations regardless of age.

BMW i8 Insurance Costs

The BMW i8 occupies a unique position in the sports car market because it combines exotic styling with hybrid technology.

Insurance premiums often range from:

- $3,000–$6,500 annually

- $250–$550 monthly

The i8's insurance costs are influenced by:

- High original purchase price

- Specialized hybrid components

- Carbon-fiber construction

- Limited production volume

- Advanced technology systems

Although the BMW i8 is not the most powerful sports car in its class, its repair costs can be substantial due to its complex engineering and unique materials.

For example, damage to carbon-fiber components may require specialized repairs that are significantly more expensive than repairs on traditional steel-bodied vehicles.

Buyers considering a used i8 should obtain insurance quotes before purchasing, as premiums can vary widely among insurers.

Jaguar F-Type Insurance Costs

The Jaguar F-Type combines luxury and performance in a package that often commands above-average insurance rates.

Typical premiums commonly fall between:

- $2,800–$6,000 per year

- $235–$500 per month

Insurance companies consider several factors when pricing F-Type coverage:

- Luxury vehicle classification

- Expensive replacement parts

- Performance-oriented engines

- Higher repair labor costs

- Relatively limited parts availability

Models equipped with supercharged V8 engines generally cost more to insure than four-cylinder or V6 variants.

The Jaguar brand's luxury positioning can also increase claim costs because repairs often require specialized service facilities.

While used F-Type models may offer attractive purchase prices, buyers should factor insurance and maintenance expenses into their long-term ownership plans.

Tesla Model S Plaid Insurance Costs

The Tesla Model S Plaid is one of the fastest production sedans available today, and its insurance costs often reflect its extraordinary performance capabilities.

Many owners pay approximately:

- $3,500–$7,500 annually

- $300–$625 monthly

for full coverage.

Several factors contribute to these premiums:

- Extremely rapid acceleration

- High vehicle value

- Advanced electronics

- Expensive battery systems

- Costly repair procedures

Despite its excellent safety ratings, the Model S Plaid can be expensive to insure because even relatively minor collisions may involve costly repairs.

For example, repairing:

- Battery-related components

- Cameras

- Sensors

- Body panels

can result in substantial claim payouts.

Tesla's specialized repair network and parts availability can also influence insurance pricing.

As electric performance vehicles become more common, insurance costs may evolve, but the Plaid currently remains one of the more expensive vehicles to insure.

Mercedes-AMG GT Insurance Costs

The Mercedes-AMG GT represents the luxury performance segment at its highest level and often carries some of the most expensive insurance premiums among non-exotic sports cars.

Typical insurance costs often range between:

- $4,000–$9,000+ per year

- $335–$750+ per month

depending on:

- Model year

- Vehicle value

- Driver profile

- Coverage levels

The AMG GT's premiums are influenced by:

- High horsepower ratings

- Luxury vehicle status

- Expensive replacement parts

- Sophisticated technology systems

- High repair costs

Insurance companies recognize that accidents involving AMG GT models often generate large claims because repairs require specialized parts and labor.

Higher-performance AMG variants can push premiums even further upward.

For many buyers, insurance becomes one of the largest recurring ownership expenses associated with this vehicle.

Which Sports Cars Have the Cheapest Insurance?

Many people assume that every sports car comes with expensive insurance. While this is true for some high-performance and luxury models, there are several sports cars that offer relatively affordable insurance rates.

Insurance companies generally charge less for vehicles that have:

- Moderate horsepower

- Strong safety ratings

- Lower repair costs

- Affordable replacement parts

- Lower claim severity

For budget-conscious buyers, choosing one of these models can significantly reduce total ownership costs. In some cases, the insurance savings over several years can amount to thousands of dollars compared to more powerful performance vehicles.

The following sports cars are often among the least expensive to insure in the United States.

Mazda MX-5 Miata

The Mazda MX-5 Miata is consistently one of the cheapest sports cars to insure.

Many drivers pay approximately:

- $1,500–$2,500 per year

- $125–$210 per month

for full coverage insurance.

Several factors contribute to the Miata's affordability:

- Relatively modest horsepower

- Lightweight construction

- Strong reliability record

- Reasonable repair costs

- Lower purchase price than many competitors

Unlike many sports cars, the Miata focuses more on handling and driving enjoyment than outright speed.

Insurance companies generally view it as a lower-risk performance vehicle because it produces fewer costly claims than many larger sports cars.

For example, a buyer comparing a used Miata and a Chevrolet Corvette may discover that the Miata costs significantly less to insure while still providing an engaging driving experience.

This combination of fun and affordability makes it one of the most popular choices for budget-minded enthusiasts.

Toyota GR86

The Toyota GR86 is another sports car that often delivers surprisingly affordable insurance rates.

Typical premiums frequently range between:

- $1,700–$2,800 annually

- $140–$230 monthly

The GR86 benefits from several characteristics insurers like:

- Moderate engine output

- Relatively low vehicle value

- Good safety equipment

- Affordable replacement parts

- Lower repair expenses than luxury sports cars

Although the GR86 is designed for performance driving, it is not associated with the extreme horsepower levels found in many muscle cars and high-performance vehicles.

For example, a Toyota GR86 often costs considerably less to insure than:

- Chevrolet Corvette

- Porsche 911

- Dodge Challenger Scat Pack

For buyers who want a modern sports coupe without overwhelming insurance expenses, the GR86 is often one of the strongest options available.

Subaru BRZ

The Subaru BRZ shares much of its design and engineering with the Toyota GR86, which means insurance costs are usually similar.

Many drivers pay approximately:

- $1,800–$3,000 per year

- $150–$250 per month

for full coverage.

Insurance companies generally view the BRZ favorably because of its:

- Moderate horsepower

- Lower replacement cost

- Strong safety technologies

- Reasonable repair costs

Compared with V8-powered muscle cars, the BRZ often presents less risk from an insurance perspective.

For example, a young driver may find that a BRZ costs substantially less to insure than a Ford Mustang GT or Chevrolet Camaro SS.

This makes the BRZ particularly appealing to first-time sports car owners who want manageable ownership costs.

Ford Mustang EcoBoost

Not every Mustang is expensive to insure.

While V8-powered Mustang GT models often carry higher premiums, the Mustang EcoBoost is frequently among the more affordable performance cars in its class.

Typical insurance costs often range from:

- $1,800–$3,200 annually

- $150–$270 monthly

Several factors help keep costs lower than many performance-oriented Mustang variants:

- Smaller turbocharged engine

- Lower purchase price

- Reduced claim severity

- Lower repair costs than some V8 models

The EcoBoost version allows buyers to enjoy:

- Sporty styling

- Strong acceleration

- Modern technology

- Everyday practicality

without facing the insurance costs often associated with larger-engine muscle cars.

For many drivers, the EcoBoost represents a practical compromise between performance and affordability.

Factors That Make Some Sports Cars Cheaper to Insure

Not all sports cars are priced the same by insurance companies. Certain characteristics consistently lead to lower premiums.

Some of the most important factors include:

Moderate Horsepower

Vehicles with moderate power outputs generally present less risk than cars capable of extreme acceleration and very high speeds.

For example:

- Toyota GR86

- Subaru BRZ

- Mazda MX-5 Miata

typically cost less to insure than high-horsepower muscle cars.

Lower Vehicle Value

Less expensive vehicles usually require smaller claim payouts if they are stolen or declared a total loss.

This reduces risk for insurers and often results in lower premiums.

Affordable Repair Costs

Sports cars that use widely available parts and conventional repair procedures tend to cost less to insure.

Vehicles requiring specialized parts or highly skilled labor generally generate larger claims.

Strong Safety Ratings

Advanced safety systems and strong crash-test performance can help lower insurance costs by reducing accident severity.

Features such as:

- Automatic emergency braking

- Lane-departure warnings

- Blind-spot monitoring

may contribute to lower premiums.

Lower Theft Rates

Vehicles that are stolen less frequently typically receive lower comprehensive insurance rates.

Insurers carefully monitor theft statistics when calculating premiums.

Driver Demographics

Some sports cars attract older and more experienced owners who generally file fewer claims.

This can positively influence insurance pricing for specific models.

Which Sports Cars Are the Most Expensive to Insure?

While some sports cars have surprisingly affordable insurance premiums, others sit at the opposite end of the spectrum. High-performance vehicles, luxury sports cars, and exotic models often generate some of the highest insurance costs on the road.

Insurance companies charge more for these vehicles because they typically involve:

- Higher repair costs

- Larger claim payouts

- More expensive replacement parts

- Greater theft risk

- Higher accident severity

For budget-conscious buyers, understanding which vehicles tend to have the highest premiums can help prevent costly surprises. In some cases, insurance costs can add thousands of dollars per year to the total cost of ownership.

High-Horsepower Performance Cars

One of the biggest factors driving insurance costs is horsepower.

Vehicles with extremely powerful engines often cost significantly more to insure because insurance companies associate them with:

- Faster acceleration

- Higher speeds

- Increased accident severity

- Larger claim payouts

Examples of high-horsepower performance cars that frequently carry elevated insurance premiums include:

- Dodge Challenger Hellcat

- Chevrolet Camaro ZL1

- Ford Mustang Shelby GT500

- Chevrolet Corvette Z06

- Cadillac CT5-V Blackwing

Many of these vehicles produce:

- 500 horsepower

- 600 horsepower

- 700 horsepower or more

Insurance companies recognize that accidents involving these vehicles can be particularly expensive.

For example, a Dodge Challenger Hellcat may cost substantially more to insure than a Mustang EcoBoost, even if both are driven by the same person.

The difference often comes down to risk statistics and claim history.

Buyers attracted to high-performance models should always obtain insurance quotes before purchasing because premiums can sometimes exceed expectations.

Luxury Sports Cars

Luxury sports cars combine performance with premium materials, advanced technology, and higher vehicle values.

As a result, they often generate higher insurance costs than mainstream sports cars.

Examples include:

- Porsche 911

- Jaguar F-Type

- BMW i8

- Mercedes-AMG GT

- Audi R8

Several factors contribute to higher premiums:

- Expensive body panels

- Advanced electronic systems

- Specialized repair procedures

- High replacement values

- Luxury-brand repair costs

For example, repairing a Porsche 911 after a collision may cost significantly more than repairing a Toyota GR86 because:

- Parts are more expensive.

- Labor requirements are greater.

- Specialized technicians may be required.

Insurance companies account for these costs when calculating premiums.

Even drivers with excellent records often face higher rates simply because the vehicle itself represents a larger financial risk.

Exotic and Supercars

Exotic vehicles and supercars typically occupy the highest insurance category.

Examples include:

- Lamborghini Huracán

- Ferrari 296 GTB

- Ferrari F8 Tributo

- McLaren 750S

- Aston Martin Vantage

- Lamborghini Revuelto

Insurance premiums for these vehicles can easily exceed:

- $10,000 per year

- $15,000 per year

- $20,000+ per year

depending on:

- Driver profile

- Location

- Coverage limits

- Vehicle value

Several characteristics make these vehicles expensive to insure:

- Extremely high purchase prices

- Limited-production parts

- Specialized repair facilities

- Exceptional performance capabilities

- High theft attractiveness

For example, a minor collision involving a supercar may result in repair bills that exceed the total value of many ordinary vehicles.

Some insurers even require specialized policies for exotic vehicles because traditional auto insurance products may not adequately address their unique risks.

Fortunately, most budget-conscious buyers shopping through online auto auctions are unlikely to consider vehicles in this category due to both purchase and ownership costs.

Vehicles With High Theft Rates

Insurance costs are influenced not only by performance but also by theft statistics.

Some sports cars are stolen more frequently than others, which increases the risk for insurance companies.

When a vehicle has a history of frequent theft claims, insurers often raise comprehensive coverage premiums.

Examples of factors that increase theft-related insurance costs include:

- High demand for parts

- Strong resale value

- Popularity among thieves

- Ease of resale in illegal markets

Certain versions of vehicles such as:

- Dodge Challenger

- Dodge Charger performance models

- Chevrolet Camaro

- Ford Mustang

have historically appeared on theft-related reports more frequently than many ordinary passenger vehicles.

Even if an owner takes precautions, insurance companies still consider overall theft data when calculating rates.

Vehicles equipped with:

- Tracking systems

- Immobilizers

- Anti-theft devices

- Secure storage

may qualify for discounts, but theft risk remains an important factor in sports car insurance pricing.

Lower Your Total Sports Car Ownership Cost

Choosing the right vehicle is one of the easiest ways to reduce long-term expenses. BidNDrive gives buyers access to used sports cars that can cost significantly less than dealership inventory while still delivering the driving experience they want.

- ✅ Lower purchase prices through online auctions

- ✅ Popular models like Mustang, BRZ, GR86, and Miata

- ✅ Transparent auction and service fees

- ✅ Support throughout the buying process

How Much Coverage Do You Need for a Sports Car?

Choosing the right amount of insurance coverage is just as important as choosing the right sports car. While many drivers focus on finding the lowest premium, inadequate coverage can become extremely expensive after an accident, theft, or major vehicle damage.

The ideal coverage depends on factors such as:

- Vehicle value

- Driver age

- Financial situation

- State requirements

- Loan or lease obligations

- How often the vehicle is driven

For example, a driver who purchases a used Mazda MX-5 Miata for $15,000 may need a different coverage strategy than someone insuring a new Porsche 911 worth more than $120,000.

Understanding each type of coverage can help sports car owners balance protection and affordability.

Liability Insurance

Liability insurance is the foundation of every auto insurance policy and is required in most states.

This coverage pays for damages and injuries you cause to other people if you are responsible for an accident.

Liability insurance typically includes:

- Bodily injury liability

- Property damage liability

For example, if you accidentally hit another vehicle and cause injuries, liability coverage may help pay for:

- Medical expenses

- Vehicle repairs

- Legal costs

- Settlement claims

State minimum requirements are often relatively low.

However, sports car owners may benefit from higher liability limits because serious accidents can generate substantial costs.

For example, a driver causing a multi-vehicle accident could face expenses far beyond minimum state coverage requirements.

Many insurance professionals recommend purchasing liability limits that exceed the legal minimum whenever possible.

Comprehensive Coverage

Comprehensive coverage protects against damage that is not caused by a collision.

Examples include:

- Theft

- Vandalism

- Fire

- Flooding

- Hail damage

- Falling objects

- Animal collisions

This coverage is particularly important for sports cars because many performance vehicles are attractive targets for thieves.

For example, a Dodge Challenger, Chevrolet Camaro, or Ford Mustang may be more vulnerable to theft than an average commuter vehicle.

If a sports car is stolen and not recovered, comprehensive coverage may help pay for its value.

Owners of newer or higher-value sports cars generally benefit from maintaining comprehensive coverage.

Collision Coverage

Collision coverage pays for damage to your own vehicle after an accident, regardless of who caused it.

This coverage can help repair or replace your sports car after:

- Vehicle collisions

- Single-car accidents

- Impact with objects

- Rollover accidents

For example, if a driver loses control and strikes a guardrail, collision coverage may help pay for repairs.

Sports cars often have:

- Expensive body panels

- Specialized paint

- Performance components

- Advanced electronics

which can make repairs costly.

A minor accident involving a Corvette or Porsche 911 may result in repair bills that would be difficult for many owners to pay out of pocket.

For most financed sports cars, lenders require collision coverage.

Uninsured and Underinsured Motorist Coverage

Not every driver on the road carries adequate insurance.

Uninsured motorist coverage helps protect you if you are hit by a driver who has no insurance.

Underinsured motorist coverage applies when the at-fault driver's insurance limits are insufficient to cover damages.

This protection can be especially valuable because sports cars often cost more to repair than ordinary vehicles.

For example, if an uninsured driver damages a Jaguar F-Type, repair costs may exceed tens of thousands of dollars.

Without adequate coverage, the sports car owner may struggle to recover those losses.

Many drivers overlook this coverage, but it can provide important financial protection.

Personal Injury Protection (PIP)

Personal Injury Protection, commonly known as PIP, is required in some states and optional in others.

PIP helps cover medical expenses and certain related costs after an accident, regardless of who caused it.

Depending on the policy and state laws, PIP may cover:

- Medical bills

- Rehabilitation expenses

- Lost wages

- Essential services

- Funeral expenses

For example, if a driver is injured in an accident and cannot work for several weeks, PIP may help offset some of the financial burden.

This coverage is especially valuable for individuals who depend heavily on their income and want additional financial protection after an accident.

Medical Payments Coverage

Medical Payments Coverage, often called MedPay, helps pay medical expenses resulting from a vehicle accident.

Unlike liability insurance, MedPay focuses on medical costs for:

- The driver

- Passengers

- Family members in some situations

Covered expenses may include:

- Emergency treatment

- Hospital bills

- Ambulance fees

- Surgery costs

- Follow-up care

MedPay can complement health insurance and provide additional protection after an accident.

For sports car owners who frequently carry passengers, this coverage can offer added peace of mind.

Gap Insurance

Gap insurance is particularly important for owners of newer sports cars that are financed.

When a vehicle is totaled, standard insurance generally pays only the current market value.

However, the remaining loan balance may be higher than that value.

Gap insurance covers the difference between:

- The vehicle's actual cash value

- The remaining loan balance

For example:

- Loan balance: $45,000

- Insurance payout: $38,000

Without gap insurance, the owner could still owe $7,000 on a vehicle that no longer exists.

Sports cars often depreciate quickly during the first few years of ownership, making gap insurance especially valuable for financed vehicles.

New Car Replacement Coverage

Some insurers offer new car replacement coverage for recently purchased vehicles.

Instead of paying only the depreciated value of a totaled vehicle, this coverage may help replace it with a new vehicle of similar type and equipment.

For example, if a one-year-old Nissan Z is declared a total loss, new car replacement coverage may provide significantly more protection than standard actual cash value coverage.

This option can be particularly attractive for buyers purchasing:

- New sports cars

- Recently released models

- Vehicles with rapid depreciation

Although it increases premiums, some owners consider the extra protection worthwhile.

Agreed Value Coverage for Collector Sports Cars

Collector and specialty sports cars often require a different insurance approach.

Standard insurance policies typically use actual cash value, which accounts for depreciation.

However, collector vehicles may appreciate over time.

Agreed value coverage allows the owner and insurer to establish a specific value for the vehicle before a loss occurs.

Examples of vehicles that may benefit from agreed value coverage include:

- Classic Corvettes

- Vintage Porsche models

- Rare muscle cars

- Limited-production sports cars

For example, if a collector-owned Porsche has an agreed value of $150,000, that amount may be paid if the vehicle is declared a total loss, subject to policy terms.

This type of coverage helps protect owners from disputes over market value after a claim.

Sports Car Insurance for Young Drivers

For many young drivers, owning a sports car is a dream. Vehicles like the Ford Mustang, Toyota GR86, Subaru BRZ, and Mazda MX-5 Miata offer exciting performance and sporty styling at relatively affordable purchase prices. However, insurance is often where the real financial challenge begins.

Drivers under 25 generally face the highest insurance premiums in the market, especially when insuring sports cars. While this may seem unfair to responsible young drivers, insurance companies base rates on statistical risk rather than individual intentions.

The good news is that some sports cars are much cheaper to insure than others, and there are several ways young drivers can reduce their premiums without giving up the vehicle they want.

Why Drivers Under 25 Pay More

Age is one of the most important factors insurance companies use when calculating premiums.

According to insurance industry data, younger drivers are statistically more likely to:

- Be involved in accidents

- File insurance claims

- Receive traffic citations

- Engage in risky driving behavior

Because of this, insurers consider drivers under 25 to be higher-risk customers.

For example, a 22-year-old driver insuring a Ford Mustang GT may receive a quote that is twice as high as a quote for a 40-year-old driver with the same vehicle and coverage.

The difference is not necessarily related to the individual driver. Instead, it reflects accident and claim patterns across millions of policyholders.

Sports cars can make the situation even more expensive because insurers also consider:

- Horsepower

- Acceleration

- Vehicle value

- Repair costs

- Theft rates

For example:

- A 22-year-old insuring a Chevrolet Corvette may face significantly higher premiums than

- A 22-year-old driving a Toyota Camry.

This combination of youth and vehicle performance is one reason sports car insurance can become a major expense for younger drivers.

The Most Affordable Sports Cars for Young Drivers

Not every sports car comes with extreme insurance costs.

Some models are generally more affordable because they combine sporty performance with reasonable repair costs and moderate horsepower levels.

Popular options often include:

- Mazda MX-5 Miata

- Toyota GR86

- Subaru BRZ

- Ford Mustang EcoBoost

- Hyundai Veloster N

These vehicles typically cost less to insure than:

- Dodge Challenger Hellcat

- Chevrolet Camaro ZL1

- Porsche 911

- Mercedes-AMG GT

For example, a young driver may find that a used Mazda MX-5 Miata costs hundreds or even thousands of dollars less per year to insure than a high-horsepower V8 muscle car.

The Toyota GR86 and Subaru BRZ are also popular among younger enthusiasts because they provide:

- Rear-wheel-drive handling

- Sporty styling

- Reasonable purchase prices

- Manageable insurance costs

Similarly, the Mustang EcoBoost often offers lower premiums than Mustang GT models because of its smaller engine and lower claim severity.

For buyers shopping on a budget, these vehicles can provide a more realistic path to sports car ownership.

Tips for Lowering Insurance Costs as a New Driver

Although younger drivers cannot change their age, they can take several steps to reduce insurance costs.

Choose a Lower-Risk Sports Car

Vehicle selection matters.

For example, a Mazda MX-5 Miata or Toyota GR86 will often cost less to insure than a Corvette or Challenger Hellcat.

Obtaining insurance quotes before purchasing a vehicle can prevent expensive surprises.

Maintain a Clean Driving Record

Avoiding accidents and traffic violations remains one of the most effective ways to lower premiums.

Insurance companies reward drivers who demonstrate safe driving habits over time.

Even a single speeding ticket can increase rates significantly.

Increase Your Deductible

Choosing a higher deductible can lower monthly insurance costs.

For example:

- A $1,000 deductible often costs less than

- A $500 deductible.

However, drivers should ensure they can comfortably afford the deductible if a claim occurs.

Stay on a Family Policy When Possible

Many younger drivers save money by remaining on a parent's insurance policy.

In many cases, this option produces substantially lower premiums than purchasing an individual policy.

Ask About Discounts

Many insurers offer discounts for:

- Good students

- Defensive driving courses

- Safe driving programs

- Multi-policy bundles

- Low annual mileage

These savings can add up over time.

Limit Annual Mileage

Drivers who use a sports car only occasionally may qualify for lower premiums.

For example, driving 6,000 miles per year generally presents less risk than driving 18,000 miles annually.

Consider a Used Sports Car

Older sports cars often have lower replacement values, which can reduce insurance costs.

A used Subaru BRZ purchased through an online auto auction may be significantly cheaper to insure than a brand-new model while delivering a similar driving experience.

Sports Car Insurance for Used Vehicles

Many buyers assume that every sports car comes with expensive insurance premiums. However, used sports cars are often much more affordable to insure than their brand-new counterparts. In some cases, buying a used performance vehicle can reduce both the purchase price and the ongoing insurance costs.

For budget-conscious buyers, this can make sports car ownership far more realistic. Instead of paying for a new Corvette, Mustang, or Porsche, many drivers choose older models that still offer strong performance while generating lower insurance premiums.

Understanding how insurers evaluate used sports cars can help buyers identify vehicles that deliver both excitement and long-term affordability.

Is It Cheaper to Insure a Used Sports Car?

In many cases, yes.

Used sports cars often cost less to insure because they are worth less than new vehicles.

Insurance companies consider several factors when calculating premiums, including:

- Vehicle value

- Repair costs

- Replacement costs

- Theft risk

- Historical claims data

When a vehicle's market value decreases over time, the potential payout for a total loss also decreases.

For example:

- A brand-new Chevrolet Corvette worth $80,000 may cost significantly more to insure than

- A 10-year-old Corvette worth $30,000.

The same principle applies to vehicles such as:

- Ford Mustang

- Nissan Z

- Subaru BRZ

- Mazda MX-5 Miata

Although performance characteristics remain important, depreciation often helps lower insurance costs.

This is one reason many enthusiasts purchase used sports cars rather than new ones.

How Depreciation Affects Insurance Costs

Depreciation is one of the biggest reasons insurance costs often decrease as vehicles age.

Most new vehicles lose value during their first several years of ownership.

As market value declines:

- Comprehensive coverage risk decreases.

- Collision claim payouts become smaller.

- Total-loss settlements become less expensive.

For example, consider two identical sports cars separated by several model years.

A new Toyota GR86 valued at $32,000 may generate higher premiums than:

- A five-year-old GR86 valued at $20,000.

Even though both vehicles offer similar performance, the insurance company's financial exposure is lower with the older vehicle.

However, depreciation does not reduce every aspect of insurance pricing.

Other factors still matter, including:

- Driver age

- Driving history

- Location

- Theft rates

- Repair costs

A vehicle that is inexpensive to replace may still be costly to insure if it has a history of expensive claims or frequent theft.

Nevertheless, depreciation remains one of the most effective ways to reduce sports car insurance costs.

Why Auction-Bought Sports Cars May Cost Less to Insure

Many buyers use online auto auctions to find sports cars at prices below traditional dealership retail values.

Purchasing a sports car at auction does not automatically reduce insurance costs, but it can create indirect savings.

Insurance companies primarily care about:

- Vehicle value

- Vehicle condition

- Repair history

- Title status

If a buyer purchases a used sports car at a lower price because it has already depreciated significantly, insurance costs may also be lower due to the vehicle's reduced market value.

For example:

- A used Mustang purchased through an auction may have a substantially lower replacement value than a brand-new Mustang purchased from a dealership.

As a result, comprehensive and collision premiums may be lower.

Budget-conscious buyers often use auctions to purchase vehicles such as:

- Mazda MX-5 Miata

- Ford Mustang

- Chevrolet Camaro

- Nissan Z

- Subaru BRZ

at prices that make ownership more affordable.