Hot shot insurance is one of the biggest expenses for owner-operators, but choosing the right coverage can protect your business and save money in the long run. This guide explains the types of insurance you need, federal requirements, average costs, ways to lower premiums, and common mistakes to avoid so you can start or grow your hot shot trucking business with confidence.

What Is Hot Shot Trucking?

Definition of Hot Shot Trucking

Hot shot trucking is a type of freight transportation that focuses on delivering smaller, time-sensitive loads using pickup trucks instead of full-size semi-trucks. Rather than hauling large shipments in 53-foot trailers, hot shot drivers transport cargo that needs to reach its destination quickly.

The business is especially common in industries where delays are expensive. Construction companies may need replacement equipment the same day, oil and gas companies often require urgent parts, and farms may need machinery delivered during harvest season. Hot shot trucking fills the gap between local delivery services and traditional long-haul trucking.

Most hot shot businesses are operated by owner-operators who own both the truck and trailer. They typically work independently or contract with freight brokers, load boards, or direct customers.

For someone looking to start a trucking business without investing hundreds of thousands of dollars in a commercial semi-truck, hot shot trucking often appears to be a more affordable entry point. For example, a driver may purchase a used heavy-duty pickup truck and a gooseneck trailer for significantly less than the cost of a new Class 8 tractor and trailer combination.

How Hot Shot Trucking Works

The hot shot business model is built around flexibility and fast response times. Instead of following fixed routes or carrying large shipments for major carriers, hot shot drivers accept individual loads based on availability and customer demand.

A typical job follows several steps:

- A shipper or freight broker posts an available load.

- The driver reviews the pickup and delivery locations, cargo weight, and payment.

- If the load is profitable, the driver accepts the shipment.

- The cargo is picked up, secured to the trailer, and transported directly to the customer.

- After delivery, the driver receives payment according to the agreed terms.

Unlike many large trucking companies, hot shot operators often complete one shipment at a time. This allows them to move quickly without waiting for additional freight to fill a trailer.

For example, a contractor in Texas may urgently need a skid steer delivered to a job site 300 miles away. Instead of waiting for a traditional freight carrier to include the equipment in a larger shipment, a hot shot driver can transport it directly and complete the delivery the same day.

Many drivers find loads through online freight marketplaces, while others develop long-term relationships with local businesses that regularly need expedited transportation.

Types of Hot Shot Loads

Hot shot trucking covers many different types of freight. The common factor is that the shipment is relatively small but needs to arrive quickly.

Common hot shot loads include:

- Construction equipment

- Industrial machinery

- Farm equipment

- Building materials

- Auto parts

- Heavy vehicle components

- Steel products

- Pipes and tubing

- Pallets of commercial goods

- Small generators

- Compressors

- Utility equipment

- Oilfield supplies

- Recreational vehicles

- Small tractors

Some loads require special handling because of their size, weight, or value. Drivers transporting expensive machinery may need additional cargo insurance, while oversized equipment could require permits depending on state regulations.

Load weights vary significantly. Non-CDL operators generally remain below the federal weight threshold, while CDL drivers can haul much heavier cargo using larger trailers.

Common Equipment Used by Hot Shot Drivers

Although pickup trucks are the foundation of hot shot trucking, the business requires much more than just a truck.

The most common vehicle is a heavy-duty one-ton pickup, often equipped with dual rear wheels for greater towing stability. Popular choices include models such as the Ford F-350, Ram 3500, and Chevrolet Silverado 3500 HD.

Drivers usually pair these trucks with trailers designed for commercial freight. Common trailer types include:

- Gooseneck trailers

- Flatbed trailers

- Equipment trailers

- Tilt deck trailers

- Low-profile trailers

- Enclosed cargo trailers for protected freight

In addition to the truck and trailer, operators invest in equipment that helps them transport cargo safely, including:

- Ratchet straps

- Chains

- Binders

- Tarps

- Edge protectors

- Toolboxes

- Winches

- Spare tires

- Safety cones

- Fire extinguishers

Many drivers also install GPS tracking systems, dash cameras, electronic logging devices (ELDs), and trailer brake controllers to improve safety and comply with federal regulations when required.

Having reliable equipment reduces downtime and can also help lower insurance risks by preventing accidents and cargo damage.

Hot Shot Trucking vs Traditional Trucking

Although both industries transport freight, hot shot trucking operates very differently from traditional commercial trucking.

Traditional trucking companies usually move large shipments using Class 8 semi-trucks with enclosed or refrigerated trailers. Their routes are often scheduled days or weeks in advance, and shipments may include freight from multiple customers.

Hot shot trucking focuses on speed and flexibility. Drivers typically transport one customer's load directly from pickup to delivery without making multiple stops.

Some key differences include:

|

Hot Shot Trucking |

Traditional Trucking |

|

Pickup truck and trailer |

Semi-truck and large trailer |

|

Smaller loads |

Full trailer loads |

|

Faster delivery |

Scheduled freight routes |

|

Often one shipment at a time |

Multiple shipments may share trailer space |

|

Lower startup cost |

Higher equipment investment |

|

Mostly owner-operators |

Large fleets and trucking companies |

This flexibility is one reason many new business owners choose hot shot trucking. However, drivers are responsible for managing dispatching, maintenance, fuel expenses, insurance, taxes, and customer relationships on their own.

Why Owner-Operators Choose Hot Shot Trucking

Many drivers are attracted to hot shot trucking because it offers an opportunity to become self-employed without the financial commitment required to purchase a commercial semi-truck.

Instead of working for a large carrier, owner-operators can choose their own loads, set their schedules, and decide where they want to operate.

For someone starting with limited savings, the lower startup costs can make a significant difference. A driver may already own a heavy-duty pickup truck and only need to purchase a commercial trailer and obtain the necessary operating authority and insurance before entering the market.

Hot shot trucking also provides flexibility. Some drivers work full time, while others haul freight only a few days each week to supplement another source of income.

The potential to earn more by operating independently is another major advantage. Drivers who carefully manage fuel costs, maintenance expenses, insurance premiums, and load selection can build a profitable business over time.

What Is Hot Shot Insurance?

Hot shot trucking may look simpler than traditional trucking, but it is still a commercial transportation business. When a driver hauls cargo for money, personal auto insurance is not enough. Hot shot insurance helps protect the driver, the truck, the trailer, the cargo, and other people on the road if something goes wrong.

Why Hot Shot Drivers Need Insurance

Hot shot drivers need insurance because they operate vehicles for business purposes. A pickup truck used to haul paid loads is no longer just a personal vehicle. It becomes part of a commercial operation, and that changes the risk.

For example, imagine a new owner-operator buys a used dually truck to start hauling small equipment. The truck may be affordable, and the driver may try to keep startup costs low. But if that driver causes an accident while transporting a customer’s load, a personal auto policy may deny the claim. That can leave the driver responsible for vehicle damage, medical bills, legal costs, and damaged cargo.

Insurance is also required to work with many brokers, shippers, and load boards. Most customers will not release freight to a driver who cannot show proof of proper commercial coverage. Without insurance, a hot shot business may not be able to operate legally or get consistent loads.

Hot shot insurance can help cover:

- Damage caused to other vehicles

- Injuries to other people

- Damage to customer cargo

- Damage to the driver’s truck or trailer

- Theft or vandalism

- Legal costs after an accident

- Certain business-related claims

For budget-conscious drivers, insurance may feel like a large expense at first. However, one uncovered accident can cost far more than the annual premium.

Start Your Hot Shot Business Without Overpaying for Equipment

A reliable pickup truck is one of the biggest investments for any hot shot operator. BidNDrive gives you access to thousands of used heavy-duty trucks from U.S. auto auctions, helping you reduce startup costs before you hit the road.

- ✅ Access to dealer-only and public auto auctions

- ✅ Thousands of Ford, Ram, and Chevrolet trucks available

- ✅ 100% refundable deposit before bidding

- ✅ Support from bidding to vehicle pickup

How Hot Shot Insurance Differs From Regular Truck Insurance

Hot shot insurance is different from regular truck insurance because it is built for commercial hauling. A standard personal auto policy usually covers everyday driving, such as commuting, errands, or family use. It is not designed for hauling freight for payment.

Even if the vehicle is a pickup truck, the way it is used matters. A Ford F-350 used to drive to the grocery store is one type of risk. The same truck pulling a loaded gooseneck trailer across several states is a much different risk.

Hot shot insurance may include several types of coverage that regular auto insurance does not provide, such as commercial auto liability, motor truck cargo coverage, physical damage coverage, general liability, and filings required for operating authority.

Regular insurance usually focuses on the vehicle and driver. Hot shot insurance focuses on the full business activity. That includes the truck, trailer, cargo, customers, public liability, and federal or state compliance.

For example, if a driver hauls an auction vehicle for a customer and that vehicle is damaged during transport, personal auto insurance will usually not cover the customer’s loss. A proper cargo policy may help cover that type of situation, depending on the policy terms.

This is why hot shot drivers should be honest with insurance agents about how the truck is used. Trying to save money by keeping a personal policy can create serious problems later.

Risks Faced by Hot Shot Trucking Businesses

Hot shot trucking comes with many risks, even for careful drivers. The business often involves long hours, tight delivery windows, heavy trailers, changing weather, unfamiliar roads, and valuable cargo.

One of the biggest risks is a road accident. A loaded truck and trailer need more time to stop than a regular pickup. If traffic suddenly slows down, the driver may not have enough space to avoid a collision.

Cargo damage is another common risk. Loads can shift, straps can loosen, and equipment can be damaged by road vibration, rain, snow, or improper securement. Even a small mistake can become expensive if the cargo belongs to a customer.

Hot shot drivers also face business risks. A truck breakdown can stop income immediately. A stolen trailer can create a major financial setback. A missed delivery deadline can damage the driver’s relationship with a broker or shipper.

Common hot shot trucking risks include:

- Accidents with other vehicles

- Cargo loss or damage

- Trailer damage

- Theft of tools, equipment, or freight

- Weather-related damage

- Load securement problems

- Injury claims

- Property damage claims

- Lawsuits after an accident

- Business interruption after a breakdown

For a new driver with limited savings, these risks are especially serious. A driver may have enough money to buy a used truck and trailer, but not enough to pay for a major claim out of pocket. Insurance helps reduce that financial exposure.

Who Provides Hot Shot Insurance Coverage

Hot shot insurance is usually provided by companies that offer commercial trucking insurance. Some are large national insurance carriers, while others specialize in transportation, owner-operators, and small trucking businesses.

Drivers can buy coverage directly from some insurance companies, but many hot shot operators work with insurance agents or brokers. An insurance broker can compare quotes from multiple carriers and help the driver find coverage that matches the type of freight, truck, trailer, operating radius, and business structure.

This is important because not every insurance company understands hot shot trucking. Some providers may insure general commercial vehicles but may not offer the filings, cargo limits, or policy structure needed for interstate hauling.

A hot shot insurance provider may ask for details such as:

- Driver’s license type

- CDL status

- Driving record

- Truck year, make, and model

- Trailer type

- Gross vehicle weight rating

- Type of cargo hauled

- Operating radius

- State of operation

- Business experience

- Motor carrier authority status

- Desired coverage limits

A driver who plans to haul vehicles from auctions, for example, may need different coverage than a driver transporting construction materials. The insurance company needs these details to price the policy correctly and make sure the coverage fits the work.

Who Needs Hot Shot Insurance?

Hot shot insurance is needed by anyone who uses a truck and trailer to haul cargo for money. It does not matter if the business is large or small, new or experienced, CDL or non-CDL. Once a driver is transporting freight as a business, proper commercial coverage becomes an important part of staying legal, protecting income, and working with brokers or shippers.

Owner-Operators

Owner-operators are one of the main groups that need hot shot insurance. An owner-operator owns or leases the truck and runs the business independently. This means the driver is responsible for the vehicle, trailer, cargo, insurance, fuel, repairs, paperwork, and customer relationships.

For example, a driver may buy a used Ram 3500 and a gooseneck trailer to start hauling equipment in nearby states. The startup cost may be lower than buying a semi-truck, but the business still carries serious risk. If the driver hits another vehicle, damages a customer’s load, or loses a trailer in an accident, the financial responsibility can fall directly on the owner-operator.

Hot shot insurance helps protect the owner-operator from claims that could otherwise damage the entire business. It can also make the driver more attractive to brokers because many brokers require proof of liability and cargo coverage before assigning loads.

Independent Hot Shot Drivers

Independent hot shot drivers also need insurance because they usually work without the protection of a large carrier. Some independent drivers find loads through load boards, some work with freight brokers, and others build direct relationships with local businesses.

This independence gives drivers more control, but it also means they carry more responsibility. There may be no company safety department, no fleet manager, and no corporate insurance policy covering the operation.

An independent driver who hauls a customer’s equipment on Monday and auction vehicles on Friday needs coverage that matches the type of freight being transported. If the policy does not cover the load type, the driver may face problems during a claim.

For drivers trying to keep costs low, it can be tempting to buy only the cheapest policy available. But independent operators should focus on the right coverage first. A low monthly payment is not helpful if the policy does not cover the actual work being done.

Small Fleet Owners

Small fleet owners need hot shot insurance because they manage more than one truck, trailer, or driver. Even if the fleet has only two or three trucks, the risk is higher than a single-truck operation.

Each additional driver adds more exposure. One driver may have a clean record, while another may have less experience. One truck may stay local, while another may run interstate routes. These details can affect insurance costs and coverage needs.

Small fleet owners may need policies that cover:

- Multiple trucks

- Multiple trailers

- Hired drivers

- Cargo

- Physical damage

- General business liability

- Workers’ compensation or occupational accident coverage

- Different operating areas

For example, a business owner may start with one truck and later add a second driver after getting steady work from brokers. At that point, the insurance policy must be updated. If the new truck or driver is not listed correctly, a claim may become complicated or denied.

Small fleet owners should also pay close attention to driver qualification. A safe, experienced driver may help control insurance costs, while poor driving records can raise premiums quickly.

CDL Hot Shot Drivers

CDL hot shot drivers usually haul heavier loads or operate vehicle combinations that require a commercial driver’s license. Because these drivers may handle larger trailers, heavier cargo, and higher-value loads, their insurance needs can be more complex.

A CDL driver may use a dually pickup with a larger gooseneck trailer and haul equipment across state lines. That type of operation often requires higher liability limits, cargo coverage, and proper filings with federal or state authorities.

CDL drivers may also have access to more types of freight. Heavier equipment, construction machinery, and industrial loads can pay better, but they can also increase insurance risk. A more expensive load may require higher cargo limits. A heavier combination may increase the chance of serious damage in an accident.

For CDL hot shot drivers, insurance is not just a business expense. It is part of being accepted by brokers, staying compliant, and protecting the equipment used to earn income.

Non-CDL Hot Shot Operators

Non-CDL hot shot operators may also need hot shot insurance, even if they do not need a commercial driver’s license for their setup. This is a common area of confusion for beginners.

A driver may think, “I do not need a CDL, so I probably do not need commercial insurance.” That is not true. License requirements and insurance requirements are separate issues.

If a non-CDL operator hauls freight for money, the truck is still being used for business. Personal auto insurance usually does not cover paid hauling. The driver may still need commercial auto liability, cargo insurance, physical damage coverage, and other protections depending on the operation.

For example, someone may use a pickup and smaller trailer to deliver motorcycles, auto parts, lawn equipment, or light machinery. The total weight may stay under the CDL threshold, but the driver is still transporting customer property. If that cargo is damaged, the customer may expect payment.

Non-CDL hot shot operators should be careful not to underinsure the business. Staying below CDL weight limits may reduce some requirements, but it does not remove the need for proper commercial coverage.

New Trucking Businesses

New trucking businesses need hot shot insurance before they begin hauling freight. Insurance is often one of the first major expenses a new operator faces, and it should be included in the startup budget from the beginning.

Many beginners focus on buying the truck and trailer first. They search for a used pickup, compare trailer prices, and calculate fuel costs. But insurance can be one of the largest monthly expenses in the business, especially for new operators with no trucking history.

A new business may need insurance to:

- Activate operating authority

- Work with brokers

- Register with certain load boards

- Meet shipper requirements

- Protect the truck and trailer

- Cover cargo claims

- Stay compliant with federal or state rules

For example, a driver may buy an affordable used truck at auction to save money and start a hot shot business. That can be a smart move if the truck is inspected properly and the numbers make sense. But the driver should also check insurance quotes before buying. Some trucks, locations, driving records, and cargo types can lead to higher premiums than expected.

Planning insurance early helps prevent surprises. A low-cost truck does not help much if the monthly insurance payment makes the business unprofitable.

Drivers Operating Under Their Own Authority

Drivers operating under their own authority need hot shot insurance because they are responsible for meeting legal and business requirements directly. Operating authority means the driver or company has permission to transport freight as a motor carrier.

When a driver runs under their own authority, they are not using another carrier’s authority or insurance structure. They must arrange the proper coverage, maintain filings, keep policy information updated, and make sure coverage does not lapse.

This usually includes commercial liability insurance and may include cargo coverage, physical damage coverage, and required filings depending on the operation. Brokers and shippers will often check insurance information before offering loads.

For example, a new owner-operator may decide to get their own authority to avoid depending on another company. This can give more control and better long-term business potential. But it also means more responsibility. If the insurance policy is canceled, expires, or does not meet requirements, the driver may lose access to loads or face compliance issues.

How Hot Shot Insurance Works

Hot shot insurance works like a group of protections built around a commercial hauling business. It is not just one simple policy. Depending on the driver’s setup, it may include liability coverage, cargo coverage, physical damage coverage, federal filings, and state-required coverage. The goal is to prove that the business can pay for covered losses and operate legally when hauling freight for money. FMCSA says insurance requirements depend on entity type, operating authority, cargo type, and vehicle type.

Federal and State Insurance Requirements

Hot shot drivers may need to meet both federal and state insurance requirements. Federal requirements usually apply when a carrier transports property across state lines or operates as a for-hire motor carrier in interstate commerce. State requirements may apply to vehicle registration, intrastate hauling, local permits, minimum insurance limits, and business operation rules.

For many hot shot operators, the federal side is connected to the FMCSA. If the business hauls freight under its own authority, the company may need proof of public liability insurance on file before authority becomes active. FMCSA also states that once operating authority is granted, entities must maintain proof of insurance and designation of agents for process on file to avoid revocation proceedings.

State rules can be different from federal rules. A driver operating only inside one state may still need commercial insurance, even if federal operating authority is not required. For example, a driver hauling equipment from Dallas to Houston may not cross state lines, but the truck is still being used for business. The driver may still need commercial auto coverage and may need to meet Texas state requirements.

This is why hot shot drivers should not assume that “local only” means “no insurance rules.” The route, cargo, vehicle weight, business structure, and customer requirements all matter.

Insurance Requirements for Motor Carriers

A motor carrier is a business or person that transports goods or passengers for payment. Many hot shot businesses fall into this category when they haul freight for customers.

Insurance requirements for motor carriers are mainly designed to protect the public. If a commercial vehicle causes an accident, liability insurance helps pay for covered bodily injury, property damage, and certain public liability claims.

For property-carrying motor carriers, federal financial responsibility rules are found in 49 CFR Part 387. FMCSA’s safety planner states that Part 387 sets the minimum financial responsibility levels passenger and property motor carriers must maintain.

In simple terms, a hot shot carrier may need coverage for:

- Public liability

- Bodily injury

- Property damage

- Environmental restoration when required

- Cargo damage, depending on freight and customer requirements

- Truck and trailer physical damage if the owner wants protection for their own equipment

For example, a new owner-operator may have a pickup truck, a gooseneck trailer, and plans to haul vehicles or equipment. Before that driver can work with serious brokers, the broker may ask for proof of insurance. The broker wants to know that the carrier has enough coverage if the load is damaged or if an accident happens during transport.

The exact coverage amount can vary. Some brokers may require higher limits than the legal minimum. This is common when the cargo is valuable, time-sensitive, or difficult to replace.

How Insurance Filings Work

Insurance filings are documents submitted to the FMCSA or a state agency to prove that a carrier has the required coverage. The driver usually does not file these forms personally. In most cases, the insurance company or insurance agent submits them electronically.

For motor carriers, common federal insurance documents include forms such as the MCS-90 endorsement and BMC-91 or BMC-91X filings. FMCSA lists MCS-90 as an endorsement for motor carrier public liability policies, and notes that many insurance carriers are set up to make required filings electronically.

A filing is not the same thing as a full insurance policy. It is proof that the required coverage exists. The actual policy explains what is covered, what is excluded, what limits apply, and what deductibles the business must pay.

For example, if a hot shot driver applies for operating authority, the insurance company may submit the required liability filing to FMCSA. Once FMCSA receives and processes the filing, the authority can move closer to active status if all other requirements are met.

This step matters for new drivers. A driver may buy a truck and trailer, pay for insurance, and think they are ready to haul freight right away. But if the required filings have not been processed, the authority may not be active yet. Hauling too early can create compliance problems and may also cause issues with brokers.

When Coverage Begins and Ends

Hot shot insurance usually begins on the effective date listed in the policy. This date is important. A quote is not the same as active coverage. A payment receipt is not always enough by itself. The driver should confirm the policy is active and that the correct truck, trailer, business name, and coverage limits are listed.

Coverage may end when the policy expires, when the business cancels it, or when the insurance company cancels it according to policy rules and required notice periods. If the policy ends, the driver may lose access to brokers and loads. If required filings are canceled, operating authority can also be affected.

A coverage lapse can be expensive. Even a short gap may create problems with compliance, broker approval, and future insurance rates. For example, if a driver forgets to make a monthly payment and the policy cancels, that driver may not legally be able to haul a load the next day. If an accident happens during the gap, the business may have no protection for that claim.

Hot shot drivers should also understand that coverage may not apply to every situation. A policy may have exclusions for certain cargo, drivers, routes, or uses. For instance, a policy written for general freight may not automatically cover hauling cars, heavy equipment, or hazardous materials.

Before accepting a new type of load, the driver should check whether the policy covers that cargo. This is especially important for budget-minded drivers who are trying to take any available load to keep cash coming in. One load that is not covered can create a much bigger financial problem than turning it down.

Annual Policy Renewals and Updates

Most hot shot insurance policies renew every year. At renewal time, the insurance company reviews the business again. The new premium may go up, go down, or stay close to the same depending on the driver’s record, claims history, equipment, cargo, operating radius, and business growth.

A renewal is more than just paying for another year. It is a chance to make sure the policy still matches the business.

A hot shot operator should update the policy when there are changes such as:

- A new truck

- A new trailer

- A new driver

- A change in business address

- A larger operating radius

- A different type of cargo

- New authority status

- Higher broker insurance requirements

- A change from intrastate to interstate operations

- A change from non-CDL to CDL operations

For example, a driver may start by hauling light equipment within 100 miles. Six months later, the same driver may begin hauling vehicles from auctions across several states. That change can affect liability needs, cargo coverage, filings, and premium. If the policy is not updated, the driver may be underinsured.

Required Hot Shot Insurance Coverage

Required hot shot insurance coverage depends on how the business operates, what type of freight it hauls, where it travels, and whether the driver runs under their own authority. Some coverage is required by law or by FMCSA rules. Other coverage may be required by brokers, shippers, lenders, or trailer leasing companies. For most hot shot operators, the goal is simple: carry enough protection to stay legal, get loads, and avoid a financial disaster after one accident.

Primary Liability Insurance

Primary liability insurance is one of the most important types of hot shot insurance. It helps cover damage or injuries caused to other people when the driver is at fault in an accident.

For example, if a hot shot driver rear-ends another vehicle while hauling a trailer, primary liability may help pay for the other driver’s vehicle repairs, medical bills, and related legal claims. It does not usually pay to repair the hot shot driver’s own truck or trailer. That is handled by other coverage, such as physical damage insurance.

For many for-hire property carriers, federal financial responsibility rules apply under 49 CFR Part 387. FMCSA explains that insurance requirements depend on the type of carrier, vehicle, cargo, and authority status. For many for-hire property carriers with vehicles over 10,001 pounds GVWR, the listed public liability requirement is commonly $750,000, with higher limits for some hazardous materials and specialized operations.

Even when $750,000 is the legal minimum, many brokers prefer or require $1,000,000 in liability coverage. A new driver trying to get better loads may find that meeting broker requirements is just as important as meeting the legal minimum.

Commercial Auto Liability Coverage

Commercial auto liability coverage protects the business when a vehicle is used for paid hauling. This is different from personal auto insurance. A pickup truck used to pull a trailer for customers is a commercial vehicle in the eyes of insurers, even if the truck looks like a regular pickup.

Commercial auto liability usually applies when the insured truck is being used for business operations. It can help cover third-party injury and property damage claims after a covered accident.

For example, a driver may buy a used Ford F-350 to save money and start hauling small equipment. If that truck is insured only under a personal policy, the insurer may deny a claim after learning that the truck was being used to transport freight for payment. Commercial auto liability is designed for that business use.

This coverage is especially important for drivers who haul across state lines, work with brokers, or operate under their own authority. It gives brokers and shippers proof that the driver has a real commercial policy, not just a personal truck policy.

Cargo Insurance Requirements

Cargo insurance helps cover the customer’s freight if it is damaged, lost, stolen, or destroyed during transport. For hot shot drivers, this can be very important because many loads are expensive. A small trailer may carry a vehicle, machinery, generators, building materials, or auto parts worth thousands of dollars.

Cargo insurance is not always federally required for every type of property carrier. FMCSA cargo insurance filing requirements mainly apply to household goods motor carriers and household goods freight forwarders. However, brokers and shippers often require cargo coverage before they will give loads to a carrier.

In real life, this means a hot shot driver may not be legally required to file cargo insurance with FMCSA for general freight, but still may need cargo coverage to work. A broker may require $100,000 in cargo insurance, while certain loads may need more.

For example, a driver hauling a $45,000 auction vehicle should not assume a basic cargo policy covers every situation. Some policies may exclude vehicles, used equipment, personal items inside vehicles, or certain high-value freight unless added correctly. Before accepting a load, the driver should make sure the cargo type is covered.

Physical Damage Coverage

Physical damage coverage helps protect the driver’s own truck and trailer. It is usually not the same as liability insurance. Liability protects other people. Physical damage protects the equipment the driver owns or finances.

This coverage may include collision and comprehensive protection. Collision can help pay for repairs if the truck or trailer is damaged in a crash. Comprehensive may help cover theft, vandalism, fire, hail, falling objects, or certain weather-related losses.

For budget-conscious hot shot drivers, physical damage coverage can feel optional, especially if the truck is older. But skipping it can be risky. If the truck is totaled and there is no physical damage coverage, the driver may lose the main tool used to earn income.

For example, a driver buys a used dually at auction to keep startup costs low. The truck is paid off, so there is no lender forcing physical damage coverage. But if the truck is stolen from a hotel parking lot during a route, the business may stop immediately. Physical damage coverage can help reduce that risk.

If the truck or trailer is financed, the lender will usually require physical damage coverage until the loan is paid off.

Uninsured and Underinsured Motorist Coverage

Uninsured and underinsured motorist coverage helps protect the driver when another person causes an accident but does not have enough insurance to pay for the damage. This can be important for hot shot operators because they spend many hours on the road and face more exposure than the average personal driver.

Uninsured motorist coverage may apply when the at-fault driver has no insurance. Underinsured motorist coverage may apply when the at-fault driver has insurance, but the limit is too low to cover the full loss.

For example, a hot shot driver may be hit by a driver who only carries minimum personal auto limits. The hot shot truck may be expensive to repair, the trailer may be damaged, and the driver may lose income while the equipment is down. If the other driver’s policy is not enough, uninsured or underinsured motorist coverage may help, depending on the policy and state rules.

This coverage is not always the first thing new operators think about, but it can be valuable. A driver can do everything right and still be hit by someone who is not properly insured.

Bodily Injury and Property Damage Liability

Bodily injury and property damage liability are the core parts of public liability coverage.

Bodily injury liability helps cover injury-related costs for other people when the hot shot driver is at fault. This may include medical bills, lost wages, legal expenses, and settlements.

Property damage liability helps cover damage to someone else’s property. This may include another vehicle, a fence, a building, road signs, or other property damaged in an accident.

For example, if a driver loses control while pulling a loaded gooseneck trailer and hits another vehicle plus a roadside barrier, the claim may include both bodily injury and property damage. Without enough liability coverage, the driver or business may be responsible for costs above the policy limit.

For hot shot operators, these limits matter because truck-and-trailer accidents can become expensive quickly. A heavier vehicle can cause more damage than a regular passenger car. That is why many carriers, brokers, and shippers pay close attention to liability limits before doing business with a driver.

Additional Hot Shot Insurance Coverage Options

Required insurance gives a hot shot business a basic layer of protection, but it may not cover every risk. Many drivers add extra coverage based on the type of freight they haul, how often they work, whether they own or lease equipment, and how much financial risk they can handle. These optional coverages can increase monthly costs, but they may also protect the business from losses that a basic policy does not cover.

General Liability Insurance

General liability insurance helps protect a hot shot business from certain claims that are not directly caused by driving the truck. It may cover things like customer injuries, property damage away from the vehicle, or claims related to normal business operations.

For example, a driver may visit a customer’s yard to pick up equipment. While loading or checking paperwork, the driver accidentally damages a gate, fence, or customer-owned item. Commercial auto insurance may not apply if the damage is not directly tied to a covered vehicle accident. General liability may help in this type of situation, depending on the policy.

This coverage can be useful for owner-operators who meet customers in person, visit job sites, enter warehouses, or work directly with businesses. It is also helpful for drivers who want to look more professional when working with brokers or larger shippers.

Non-Trucking Liability Insurance

Non-trucking liability insurance helps cover liability when a truck is being used for non-business purposes. This coverage is usually more common for drivers leased to a motor carrier, but some hot shot operators may still hear about it when comparing policies.

For example, a driver may finish a delivery and use the truck to go to dinner, visit a store, or drive home without hauling a load. If an accident happens during personal use, non-trucking liability may help cover third-party injury or property damage claims.

This coverage does not usually apply while hauling freight, driving to pick up a load, or operating for business. That is why it is important to understand the difference between business use and personal use.

A new driver should not assume non-trucking liability can replace primary liability. It cannot. It is an extra coverage for a specific situation.

Trailer Interchange Insurance

Trailer interchange insurance protects a trailer that belongs to someone else while it is in the driver’s care under a trailer interchange agreement. This coverage is more common when drivers pull trailers they do not own.

For example, a hot shot driver may agree to use a customer’s trailer or a partner company’s trailer for a specific job. If that trailer is damaged in a covered accident, trailer interchange insurance may help pay for repairs or replacement, depending on the policy.

This coverage is not always needed by hot shot drivers who only use their own trailers. But it can be important for operators who work with other carriers, customers, or companies that provide trailers.

Before using someone else’s trailer, the driver should ask two questions: Who is responsible if the trailer is damaged? And does the current policy cover that trailer? Without the right coverage, a simple trailer damage claim can become a major out-of-pocket expense.

Bobtail Insurance

Bobtail insurance helps cover liability when a truck is being driven without a trailer attached, usually outside of active dispatch or business hauling. Like non-trucking liability, it is often used by drivers leased to a motor carrier.

For example, a driver may drop off a trailer and then drive the truck alone to a repair shop or parking location. If an accident happens while the truck is “bobtailing,” this coverage may apply.

In hot shot trucking, the term can be confusing because many drivers use pickup trucks rather than semi-trucks. Still, the idea is similar: the truck is moving without the trailer or not under a covered load.

Drivers should ask their insurance agent whether bobtail coverage is needed for their exact operation. Some owner-operators under their own authority may not need a separate bobtail policy if their commercial auto policy already covers the truck properly.

Rental Reimbursement and Downtime Coverage

Rental reimbursement and downtime coverage can help when a covered accident takes the truck out of service. This is important because hot shot drivers depend on their equipment to earn income.

Rental reimbursement may help pay for a temporary replacement vehicle after a covered loss. Downtime coverage may help replace some lost income while the insured truck is being repaired.

For example, a driver may have a steady route hauling equipment three times a week. If the truck is damaged in an accident and sits in the repair shop for two weeks, the driver loses income immediately. Fuel costs stop, but insurance payments, loan payments, parking, phone bills, and other business expenses may continue.

This coverage can be especially useful for small operators with limited savings. A short period without the truck can hurt cash flow. However, drivers should read the limits carefully. Some policies only pay a certain amount per day and only for a limited number of days.

Occupational Accident Insurance

Occupational accident insurance can help cover medical expenses, disability benefits, or accidental death benefits if an independent driver is injured while working. It is often used by owner-operators who are not covered by traditional workers’ compensation.

For example, a driver may slip while securing a load, fall from a trailer, or get injured while using chains and binders. Health insurance may not cover everything, and the driver may be unable to work for weeks. Occupational accident coverage may help reduce the financial impact.

This coverage is important because many hot shot drivers work alone. If they get hurt, there may be no paid sick leave, no employer benefits, and no backup income.

Occupational accident insurance does not replace every type of coverage, and it is not the same as workers’ compensation. Still, it can be a practical option for independent operators who want protection but do not have employees.

Workers' Compensation Insurance

Workers’ compensation insurance helps cover employees who are injured while working. It may pay for medical treatment, lost wages, rehabilitation, and other benefits required by state law.

A single owner-operator with no employees may not always be required to carry workers’ compensation, depending on the state and business structure. But once a hot shot business hires drivers, helpers, dispatch staff, or other employees, workers’ compensation may become necessary.

For example, a small fleet owner hires a second driver to operate another truck. If that driver is injured while loading freight, the business may be responsible. Workers’ compensation coverage can help protect both the employee and the company.

Rules vary by state, so business owners should check local requirements before hiring anyone. Skipping workers’ compensation to save money can become very expensive if an employee gets hurt.

Business Owner's Policy

A business owner’s policy, often called a BOP, combines several types of business protection into one package. It may include general liability, business property coverage, and other small business protections.

For a hot shot driver, a BOP may be useful if the business has an office, storage location, tools, computers, business equipment, or customer paperwork. It is not a replacement for commercial auto or cargo insurance, but it can protect parts of the business that trucking insurance may not cover.

For example, a driver may run dispatch and billing from a small home office or rented office space. If business equipment is stolen or damaged, a BOP may help, depending on the policy.

This type of policy is more useful as the business grows. A brand-new driver with only one truck may not need it right away, but a small fleet with an office, records, and business property may benefit from the extra protection.

Equipment and Tool Coverage

Equipment and tool coverage helps protect items used to run the business, such as chains, binders, straps, tarps, winches, ramps, toolboxes, spare parts, and hand tools.

These items may not seem expensive one by one, but replacing them all at once can cost a lot. A driver who is just starting with a tight budget may spend thousands of dollars on securement gear and basic tools before taking the first load.

For example, if a toolbox is stolen from the truck while parked overnight, standard cargo insurance may not cover it because the tools belong to the driver, not the customer. Equipment and tool coverage may help replace those business items.

This coverage is worth considering for drivers who carry expensive securement equipment or work in areas where theft is common. It can also help drivers get back to work faster after a loss.

Cyber Liability Insurance

Cyber liability insurance helps protect a business from certain losses related to data breaches, hacking, online fraud, and digital security issues. At first, this may not seem important for hot shot trucking, but many small operators now run much of their business online.

Drivers use load boards, email, digital invoices, online banking, payment apps, customer records, and cloud-based documents. If a business email is hacked or customer information is exposed, cyber liability coverage may help with response costs.

For example, a hot shot operator may receive a fake payment link or have an email account compromised. A scammer could send false payment instructions to a customer or access sensitive business information. Cyber insurance may help cover certain costs related to recovery, notification, or legal response.

This coverage may not be necessary for every one-truck operation, but it becomes more useful as the business handles more customers, payments, and digital records.

Errors and Omissions Insurance

Errors and omissions insurance, also called E&O insurance, helps protect a business from claims related to professional mistakes, missed details, or failure to provide promised services.

In hot shot trucking, this may apply in limited situations. It is more common for freight brokers, dispatch services, logistics consultants, or businesses that give professional advice. However, some hot shot businesses that arrange transportation, coordinate shipments, or provide dispatch-style services may consider it.

For example, a company may incorrectly schedule a pickup, give the wrong delivery information, or fail to communicate an important requirement. If the customer loses money and files a claim, E&O insurance may help with legal defense or covered damages.

A basic owner-operator who only hauls loads may not need this coverage at first. But if the business expands into brokering, dispatching, consulting, or managing freight for others, E&O coverage may become more relevant.

Hot Shot Insurance Requirements

Meeting hot shot insurance requirements is one of the first steps to operating a legal trucking business. The exact requirements depend on several factors, including whether the driver operates within one state or across state lines, runs under their own authority, transports regulated freight, or works through another carrier. In addition to federal and state rules, many brokers and shippers have their own insurance standards that carriers must meet before receiving loads.

Understanding these requirements before purchasing a truck or applying for operating authority can help new business owners avoid delays, unexpected expenses, and compliance issues.

Federal Insurance Requirements

Federal insurance requirements apply primarily to for-hire motor carriers that transport property in interstate commerce. If a hot shot business carries freight across state lines under its own operating authority, it generally must maintain proof of financial responsibility that meets FMCSA regulations.

Federal requirements are designed to protect the public. They ensure that if a commercial vehicle causes an accident, there is insurance available to pay covered claims involving bodily injury, property damage, or certain environmental restoration costs.

For many hot shot operators, meeting federal insurance requirements involves more than simply buying a commercial auto policy. The insurance company must also submit the appropriate filings to the FMCSA before the carrier's operating authority becomes active.

For example, a driver may purchase a used dually pickup and trailer with plans to haul equipment between Georgia and Florida. Even though the equipment is ready, the driver cannot legally begin operating under new interstate authority until all required insurance filings have been accepted by the FMCSA.

Drivers leased to another motor carrier may operate under that carrier's insurance program instead of maintaining their own federal filings. However, independent owner-operators running under their own authority are responsible for ensuring all federal insurance requirements are satisfied.

State Insurance Requirements

Every state has its own commercial vehicle insurance rules. Even drivers who never cross state lines may still need commercial insurance to operate legally.

State requirements often depend on factors such as:

- Business registration

- Vehicle weight

- Commercial vehicle classification

- Type of cargo

- Intrastate or interstate operation

- Local permitting requirements

For example, a driver who only hauls construction materials within Texas may not need interstate operating authority, but Texas still requires commercial vehicles used for business to comply with state insurance laws.

Some states also require additional filings, permits, or proof of insurance before issuing commercial registrations or operating permits.

Because state regulations vary, hot shot operators should review the requirements in every state where they plan to conduct business. This is especially important for drivers who expand from local hauling to regional operations.

FMCSA Insurance Regulations

The Federal Motor Carrier Safety Administration (FMCSA) establishes insurance regulations for many interstate motor carriers operating under federal authority.

These regulations are intended to ensure that commercial carriers have sufficient financial responsibility before transporting freight for customers.

FMCSA regulations generally address:

- Minimum public liability requirements

- Insurance filings

- Operating authority activation

- Continuous insurance coverage

- Policy cancellations

- Financial responsibility compliance

Insurance companies—not drivers—typically submit the required federal filings electronically. Once the filings are accepted and all other registration requirements are complete, the carrier's operating authority can become active.

Maintaining continuous coverage is just as important as obtaining it initially. If an insurance policy is canceled or expires, the insurance company notifies the FMCSA. If replacement coverage is not filed within the required timeframe, the carrier's operating authority may be suspended or revoked.

For new businesses, this means insurance is not a one-time purchase. It must remain active throughout the life of the company.

Minimum Liability Coverage Limits

Federal law establishes minimum public liability limits for many interstate for-hire motor carriers. The required amount depends on the type of cargo being transported.

For many property-carrying motor carriers transporting non-hazardous freight in vehicles subject to federal financial responsibility rules, the minimum public liability requirement is $750,000.

However, many hot shot drivers quickly discover that legal minimums are not always enough for doing business.

Freight brokers, logistics companies, and larger shippers often require:

- $1,000,000 in commercial auto liability coverage

- $100,000 or more in cargo insurance

- Additional insured endorsements

- Certificates of insurance

- Specific policy language

For example, a driver may technically satisfy federal requirements with the minimum liability limit. But when applying for loads through a national broker, the application may be rejected because the broker requires a $1 million liability policy.

Purchasing slightly higher liability limits can sometimes open access to more freight opportunities while providing additional financial protection after a serious accident.

Insurance Requirements for Brokers and Shippers

Legal compliance is only one part of operating a successful hot shot business. Brokers and shippers frequently establish insurance standards that exceed government requirements.

Before assigning freight, many brokers request documentation such as:

- Certificate of insurance

- Commercial auto liability limits

- Cargo insurance limits

- Active operating authority

- Safety information

- Policy effective dates

Some customers also require:

- General liability insurance

- Trailer interchange coverage

- Additional insured status

- Waivers of subrogation

- Higher cargo limits for valuable freight

For example, a manufacturer shipping expensive industrial equipment may require $250,000 in cargo insurance instead of the standard $100,000 carried by many small operators.

These additional requirements help customers reduce their own financial risk. For hot shot drivers, they are often necessary to qualify for better-paying freight.

New owner-operators should review broker requirements before purchasing insurance. Buying a policy that does not meet common broker standards may mean paying twice—once for the original policy and again for upgraded coverage.

Requirements for Interstate Operations

Interstate operations involve transporting freight across state lines or participating in interstate commerce. Once a hot shot carrier begins interstate operations under its own authority, additional federal requirements generally apply.

An interstate hot shot carrier may need to:

- Obtain FMCSA operating authority when required

- Maintain active commercial liability insurance

- Keep required insurance filings current

- Register for a USDOT number

- Comply with FMCSA safety regulations

- Meet driver qualification requirements

- Follow hours-of-service rules when applicable

- Maintain required business records

For example, a driver hauling equipment from Alabama to Tennessee is participating in interstate commerce. Even if the trip is only a few hundred miles, federal regulations may apply because the shipment crosses state lines.

Interstate carriers also need to think about future growth. A driver who initially plans to work only within one state may later receive opportunities from brokers offering loads across the Southeast. Preparing the business correctly from the beginning can make expansion much easier.

MCS-90 and BMC-91 Explained

MCS-90 and BMC-91 are two important insurance terms that many new hot shot drivers see when applying for operating authority. They are connected to federal insurance compliance, but they are not the same thing. In simple terms, the MCS-90 is an endorsement attached to an insurance policy, while the BMC-91 is a filing that proves liability coverage to the FMCSA.

What Is an MCS-90 Endorsement

An MCS-90 endorsement is a federal endorsement added to a motor carrier’s public liability insurance policy. It is required under federal regulation for motor carriers subject to FMCSA financial responsibility rules. FMCSA describes Form MCS-90 as an endorsement for motor carrier policies of insurance for public liability under the Motor Carrier Act of 1980.

The key point is that MCS-90 is not a separate insurance policy. It is added to the carrier’s liability policy. It is designed to make sure the public has financial protection if a covered motor carrier causes bodily injury, property damage, or certain environmental restoration costs.

For example, if a hot shot carrier operating under federal authority causes a serious accident while hauling freight, the MCS-90 endorsement helps show that the carrier’s policy meets federal public liability requirements.

FMCSA also notes that the MCS-90 endorsement is not issued for individual vehicles. Instead, it is attached to the motor carrier’s liability policy and applies to vehicles operated under that policy that are subject to federal financial responsibility rules.

For a new hot shot operator, this matters because adding or removing a truck from a policy can affect insurance details, but the MCS-90 itself is tied to the motor carrier’s policy, not just one specific pickup truck.

What Is a BMC-91 Filing

A BMC-91 filing is an insurance filing submitted to the FMCSA to show that a motor carrier has the required public liability insurance. It is used as proof that the carrier has coverage on file with the federal government.

In simple language, the BMC-91 tells the FMCSA: “This carrier has the required liability coverage.” Without the correct filing, a new carrier’s authority may not become active.

The BMC-91 is usually submitted by the insurance company, not by the driver. FMCSA lists BMC-91, BMC-91X, or BMC-82 as applicable forms for many motor carrier public liability insurance requirements.

For example, a driver may buy a used dually pickup and gooseneck trailer to start hauling equipment across state lines. The driver may already have a commercial auto policy, but the business still needs the correct filing submitted to the FMCSA before authority can move forward.

A BMC-91X is similar, but it is often used when coverage is provided through more than one insurance policy. A BMC-91 is typically used when the full required amount is provided under one policy.

Differences Between MCS-90 and BMC-91

The easiest way to understand the difference is this: MCS-90 is part of the insurance policy, while BMC-91 is proof filed with the FMCSA.

The MCS-90 endorsement is attached to the motor carrier’s insurance policy. It helps make sure the policy satisfies federal public liability requirements. The BMC-91 filing is sent to the FMCSA to prove that the carrier has the required insurance in place.

A hot shot driver may never personally handle these forms. The insurance company or agent usually manages them. But the driver should still understand what they mean because these filings can affect operating authority.

Here is a simple comparison:

|

Item |

What It Means |

Who Handles It |

|

MCS-90 |

Endorsement attached to the motor carrier’s liability policy |

Insurance company |

|

BMC-91 |

Filing that proves public liability insurance to the FMCSA |

Insurance company |

|

BMC-91X |

Filing used when multiple policies provide the required coverage |

Insurance company |

|

BMC-82 |

Surety bond alternative for public liability requirements |

Surety provider |

For a budget-conscious new operator, this distinction is important. A driver may think buying insurance is the final step, but the FMCSA must also receive the correct proof of coverage when federal authority is required.

When These Filings Are Required

These filings are generally required when a motor carrier must prove financial responsibility to operate under federal authority. This often applies to for-hire carriers that transport property or passengers in interstate commerce.

Hot shot drivers may need these filings if they:

- Haul freight for customers across state lines

- Operate under their own federal motor carrier authority

- Transport freight as a for-hire carrier

- Use vehicles subject to FMCSA financial responsibility rules

- Need active authority before working with brokers

FMCSA insurance requirements depend on entity type, vehicle type, cargo type, and operating authority. For example, FMCSA lists public liability requirements for for-hire property carriers and other regulated carrier types.

A driver leased to another motor carrier may not need to file under their own name if operating under that carrier’s authority and insurance structure. But a driver running independently under their own authority must make sure the proper filings are completed.

For example, someone starting a small hot shot business may plan to haul auction vehicles from Georgia to Alabama. Because the work crosses state lines and is performed for payment, federal authority and insurance filings may apply.

This is one reason new drivers should not accept loads before confirming that their authority is active. Buying a policy is not always enough. The filing must also be accepted and visible in the carrier’s FMCSA record.

How Insurance Companies Submit Filings

Insurance companies usually submit required FMCSA filings electronically. The driver or business owner provides company information, authority details, vehicle details, and policy information to the insurance agent. Then the insurance company submits the filing through the appropriate FMCSA system.

FMCSA states that many insurance carriers are set up to make required insurance filings electronically.

The process usually looks like this:

- The hot shot operator applies for commercial trucking insurance.

- The insurance company reviews the business, truck, trailer, driver, cargo, and operating radius.

- The carrier purchases the policy.

- The insurance company adds the required endorsement, such as MCS-90, when applicable.

- The insurance company submits the BMC-91 or BMC-91X filing to the FMCSA.

- The driver checks the FMCSA record to confirm that the filing has been accepted.

- The carrier waits for operating authority to become active before hauling regulated loads.

A new operator should always confirm the filing status instead of assuming everything is complete. A small paperwork delay can stop a business from booking loads.

For example, a driver may line up a profitable load for Monday, but the authority is still not active because the insurance filing has not posted yet. Taking that load too early can create compliance problems and may also make brokers unwilling to work with the carrier later.

CDL vs Non-CDL Hot Shot Insurance

CDL and non-CDL hot shot trucking can look similar from the outside. Both may use pickup trucks, trailers, and load boards. The main difference is the weight rating of the truck-and-trailer combination and the type of operation. This difference affects licensing, compliance, available loads, and insurance costs.

What Is Non-CDL Hot Shot Trucking

Non-CDL hot shot trucking means the driver operates a truck-and-trailer setup that does not require a commercial driver’s license under federal CDL rules. In many cases, this means the gross combination weight rating stays below 26,001 pounds, as long as the driver is not hauling hazardous materials or transporting passengers in a way that triggers CDL requirements. FMCSA guidance says a CDL is not required for a combination vehicle with a GCWR under 26,001 pounds, unless hazardous materials or passenger rules apply.

For example, a beginner may use a three-quarter-ton or one-ton pickup with a lighter trailer to haul small equipment, motorcycles, parts, or light freight. This can make the business easier to start because the driver may not need CDL training before operating.

However, “non-CDL” does not mean “no rules.” A non-CDL hot shot driver may still need a USDOT number, commercial insurance, broker-required cargo coverage, state permits, and proper business registration. The truck may be smaller than a semi, but it is still being used for commercial hauling.

Insurance Requirements for Non-CDL Drivers

Non-CDL hot shot drivers still need commercial insurance if they haul freight for money. A personal pickup truck policy is not designed for paid transportation work. If the driver causes an accident while hauling a customer’s load, a personal insurer may deny the claim.

A non-CDL operator may need coverage such as:

- Commercial auto liability

- Cargo insurance

- Physical damage coverage

- Trailer coverage

- General liability, depending on the business

- Uninsured and underinsured motorist coverage

For example, a driver may buy an affordable used pickup through an auction and start hauling small loads on weekends. Even if the setup stays under CDL weight limits, the business still needs proper coverage. If a customer’s equipment falls off the trailer or the driver hits another vehicle, the costs can be too high to handle out of pocket.

Some federal insurance filing requirements may also apply depending on the vehicle weight, cargo type, and authority status. FMCSA’s insurance filing table lists public liability requirements for for-hire property carriers, including different requirements for non-hazardous freight below and above 10,001 pounds GVWR.

Insurance Requirements for CDL Drivers

CDL hot shot drivers usually operate heavier truck-and-trailer combinations. This may allow them to haul larger equipment, heavier vehicles, construction machinery, or higher-paying freight. But heavier operations usually bring more compliance duties and higher insurance expectations.

A CDL hot shot driver may need:

- Primary liability insurance

- Commercial auto liability

- Cargo insurance

- Physical damage coverage

- Trailer coverage

- FMCSA filings, if operating under federal authority

- Higher cargo limits for valuable freight

- Additional coverage required by brokers or shippers

For example, a CDL driver using a dually pickup and a large gooseneck trailer may be able to haul heavier machinery than a non-CDL driver. That may create better earning opportunities, but it also increases risk. A heavier loaded trailer can cause more damage in an accident, and the cargo may be worth more.

Many brokers also view CDL operators as better suited for heavier or more complex loads. Because of that, they may require stronger insurance limits before approving the carrier.

Weight Limits and GVWR Regulations

Weight ratings are one of the most important parts of CDL vs non-CDL hot shot trucking. Drivers must understand the difference between actual weight and rated weight.

GVWR means gross vehicle weight rating. It is the maximum weight rating assigned to a truck or trailer by the manufacturer.

GCWR means gross combination weight rating. It is the combined weight rating of the truck and trailer together.

A common mistake is looking only at the actual load weight. CDL rules often look at weight ratings, not just what the truck weighs on the road that day.

For example, a pickup may have a GVWR of 14,000 pounds and the trailer may have a GVWR of 14,000 pounds. Together, the combination rating is 28,000 pounds. Even if the trailer is empty, the rated combination may place the setup into CDL territory.

FMCSA guidance states that a combination vehicle with a GCWR of 26,001 pounds or more can require a Class A CDL when the towed unit is rated over 10,000 pounds. FMCSA also explains that towed units can be added together when determining whether the 10,000-pound threshold is met.

This is why beginners should check the door sticker, manufacturer ratings, and trailer rating before buying equipment. A cheap trailer can become expensive if it pushes the business into CDL rules, higher insurance costs, and extra compliance requirements before the driver is ready.

How License Type Affects Insurance Costs

License type can affect hot shot insurance costs, but it is not the only factor. Insurance companies look at the full risk picture. They may consider the driver’s experience, driving record, CDL history, truck and trailer value, cargo type, operating radius, authority age, claims history, and location.

A non-CDL setup may sometimes cost less to insure because the truck-and-trailer combination is lighter and may haul lower-value loads. But that is not guaranteed. A new non-CDL driver with no commercial hauling experience can still receive expensive quotes.

A CDL driver may pay more if hauling heavier or more valuable freight, but a clean CDL history can also help. Insurers often like experienced drivers who can show safe commercial driving records.

For example, two drivers may both use pickup trucks for hot shot work. One is a new non-CDL operator with no business history. The other has a CDL, five years of clean commercial driving, and no claims. Even if the CDL driver hauls heavier loads, the experience may help the insurance company view that driver as a lower risk.

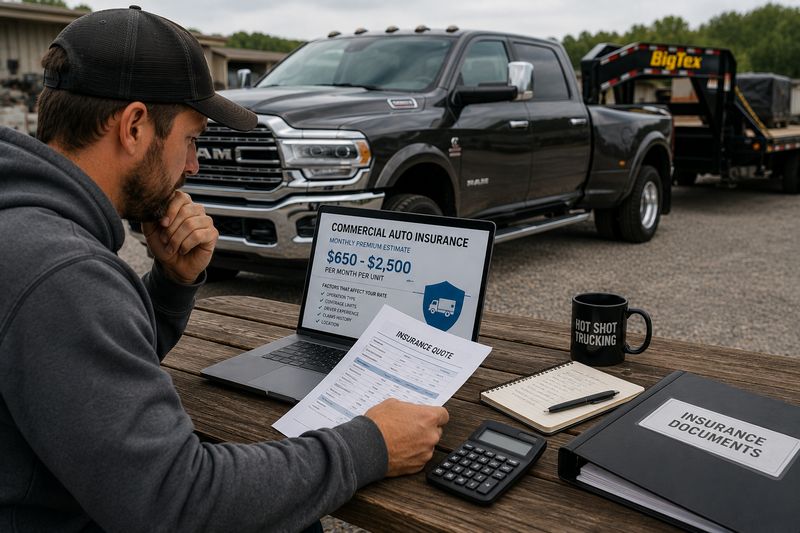

How Much Does Hot Shot Insurance Cost?

Hot shot insurance can be one of the biggest startup and monthly expenses for a new driver. The exact cost depends on the truck, trailer, cargo, location, driving record, authority status, coverage limits, and business experience. For many new operators, insurance is not a small add-on cost. It can decide whether the business is profitable or not.

Average Monthly Insurance Costs

Hot shot insurance commonly falls somewhere between $650 and $2,500 per month per unit, depending on the operation, coverage package, and driver profile. Some operators may pay less, while new businesses with higher-risk profiles may pay more. A 2025 Insureon cost analysis lists an average of $896 per month, or $10,757 per year, for hotshot truckers’ commercial auto insurance.

Progressive Commercial reported that its 2024 national average monthly cost for commercial for-hire truck insurance ranged from $746 to $954, depending on the transportation category. Progressive also notes that rates depend on factors such as inspection history, coverage requirements, vehicle type, cargo, operating radius, and driving history.

For a budget-minded driver, this means insurance should be checked before buying a truck. A pickup may look affordable at auction, but if the insurance quote is $1,800 per month, the business may need more cash flow than expected.

Annual Insurance Premiums

Annual hot shot insurance premiums often range from about $8,000 to $30,000 per year per unit, depending on coverage and risk. Some basic policies may fall below that range, while fuller packages with liability, cargo, physical damage, and extra coverages may cost more. One 2026 trucking insurance guide lists broad hot shot insurance ranges of $8,000 to $30,000 per year per unit, while another estimates motor carrier hot shot insurance at $10,000 to $30,000 per year per vehicle.

The annual number matters because monthly payments can hide the true cost. A driver paying $1,250 per month is spending $15,000 per year before fuel, repairs, tires, registration, permits, parking, accounting, and loan payments.

For example, a new owner-operator may buy a used truck to avoid a large monthly truck payment. That can help. But if the insurance premium is still $12,000 to $18,000 per year, the driver must plan enough loads to cover that expense.

Insurance Costs for New Businesses

New hot shot businesses usually pay more than experienced operators. Insurance companies see new businesses as higher risk because they have no operating history, no claims record as a carrier, and no proof that they can run safely over time.

A new business may face higher premiums because of:

- New authority

- Limited commercial driving experience

- No prior insurance history

- New cargo relationships

- Higher uncertainty for insurers

- More difficulty proving safe operations

InsuranceHub reported that hot shot insurance often ranges from $7,000 to $12,000 per year, with an average of $10,284 per year for new businesses with one truck and trailer. However, actual quotes can be much higher depending on state, coverage, driver history, and authority status.

This is why new drivers should avoid building a startup budget around the lowest quote they hear online. A safer plan is to collect several real quotes before buying equipment. That way, the driver knows whether the business can survive the first year.

Non-CDL Hot Shot Insurance Costs

Non-CDL hot shot insurance may cost less than CDL hot shot insurance in some cases because the equipment is usually lighter and the loads may be smaller. But non-CDL does not automatically mean cheap.

A non-CDL driver still uses the truck for business. The driver may still need commercial auto liability, cargo insurance, physical damage coverage, trailer coverage, and broker-required limits.

For example, someone may use a pickup and smaller trailer to haul motorcycles, small machinery, or auto parts. The setup may stay under CDL limits, but the cargo still belongs to someone else. If that cargo is damaged, the driver may need cargo insurance to respond to the claim.

Non-CDL insurance costs may be affected by:

- Truck value

- Trailer value

- Cargo type

- Operating radius

- State of business

- Driver age

- Driving record

- Coverage limits

- Whether the business has authority

- Whether physical damage is included

For a driver trying to save money, a non-CDL setup can reduce some costs, but the driver should not treat it as a loophole. Insurance companies still rate the business based on commercial risk.

CDL Hot Shot Insurance Costs

CDL hot shot insurance often costs more because CDL drivers may haul heavier freight, operate larger combinations, travel farther, and carry higher-value loads. The higher earning potential can come with higher insurance premiums.

A CDL hot shot operator may need higher liability limits, stronger cargo coverage, and additional filings if operating under their own authority. Brokers may also require more coverage before offering better-paying loads.

For example, a CDL driver hauling construction equipment with a large gooseneck trailer may be able to accept loads a non-CDL driver cannot haul. But if the cargo is worth $150,000 and the route crosses several states, the insurance company sees more risk.

CDL insurance costs can also depend heavily on experience. A CDL driver with a clean record and several years of commercial driving history may look better to insurers than a brand-new CDL holder with no hauling experience.

For drivers on a tight budget, the decision should not be based only on monthly insurance cost. A CDL setup may cost more, but it may also open access to better freight. The key is whether the extra revenue can cover the higher insurance, fuel, maintenance, and compliance costs.

Owner-Operator Insurance Expenses

Owner-operators usually carry more financial responsibility than drivers leased to a carrier. A driver leased to another carrier may operate under the carrier’s primary liability insurance, although they may still need non-trucking liability, physical damage, occupational accident coverage, or other protections.

An owner-operator running under their own authority usually pays for the full insurance package. That can include:

- Primary liability

- Cargo insurance

- Physical damage

- Trailer coverage

- General liability

- Occupational accident coverage

- Required filings

- Additional coverages required by brokers

This is why owner-operator insurance can feel expensive. The driver is not just insuring a pickup truck. The driver is insuring a business.