Looking to save money on your next car? This guide explains how to buy cars from insurance companies, including salvage and rebuilt vehicles. Learn where to find them, how to evaluate damage, and tips for safe, budget-friendly purchases. Whether you want a daily driver or a project car, this guide helps you make informed choices and get the best value at online auctions.

What Are Insurance Cars?

Insurance cars are vehicles that have been involved in incidents like accidents, theft, or natural disasters and were paid out by an insurance company. Instead of being repaired and sold through a dealer, these cars often end up at auctions, giving budget-conscious buyers a chance to purchase them at a lower price. Understanding the types of insurance cars and their history is key to making a smart purchase.

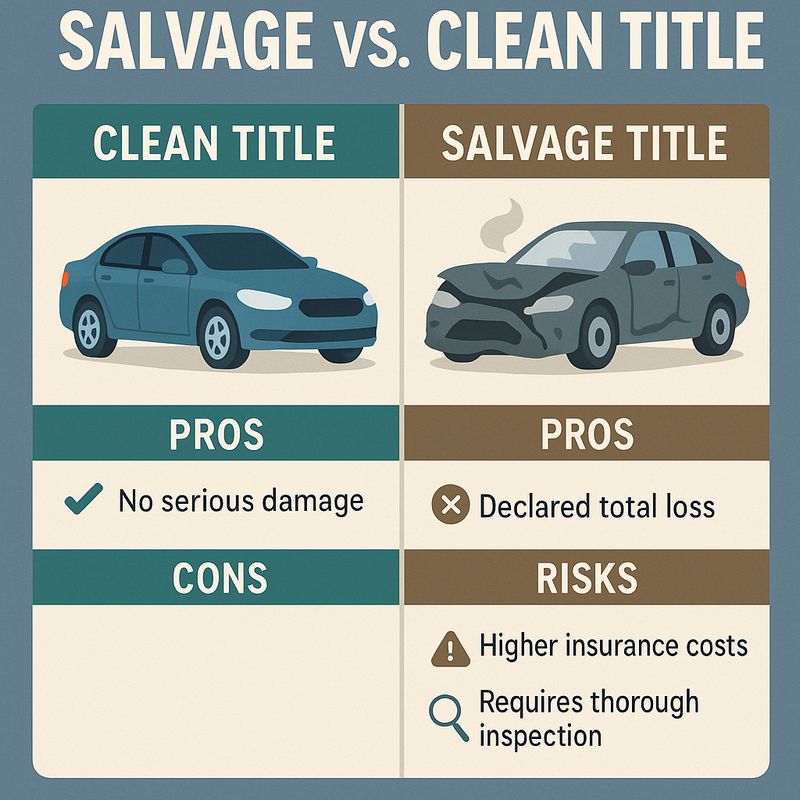

Salvage vs. Clean Title: Key Differences

A clean title indicates the car has not been seriously damaged and hasn’t been written off by an insurance company. A salvage title, on the other hand, means the car was declared a total loss by the insurer, usually due to accident, flood, or other major damage. Buyers should know that salvage cars can be repaired and legally driven, but they may have higher insurance costs and require more thorough inspection before purchase.

Why Insurance Companies Sell These Cars

Insurance companies sell these vehicles to recover some of the payout they made to the original owner. Once a car is deemed a total loss, it’s more cost-effective for the insurer to sell it at auction rather than store it indefinitely. For buyers, this creates an opportunity to purchase cars at a fraction of their market value, especially through online auction platforms like BidNDrive, which handle the process safely and efficiently.

Common Types of Insurance Vehicles (collision, theft recovery, flood, repossessed)

- Collision Damage: Cars damaged in accidents that were written off. They may have frame damage, engine issues, or cosmetic repairs.

- Theft Recovery: Vehicles that were stolen and later recovered. They can have minor damage or tampering from the theft.

- Flood Damage: Cars damaged by water due to storms or floods. These require careful inspection, as water can affect electronics and engines.

- Repossessed Vehicles: Sometimes included in insurance auctions, these are cars repossessed due to nonpayment. They usually have fewer structural issues but may have mechanical or cosmetic wear.

What Is a Salvage Vehicle?

A salvage vehicle is a car that has been damaged to the point where an insurance company declares it a total loss. These vehicles often appear at auctions, allowing buyers to purchase them at a lower price. While they can be repaired and made roadworthy, understanding salvage titles and their implications is crucial for budget-conscious buyers.

When a Car Gets a Salvage Title (total loss explanation)

A car receives a salvage title when repair costs exceed a certain percentage of its market value, typically 70–80%, depending on state laws. This can happen due to severe collisions, flood damage, fire damage, or theft recovery. The salvage designation alerts future buyers that the vehicle suffered major damage, even if it has since been repaired.

Rebuilt Title vs. Salvage Title (important distinction)

Once a salvage vehicle is repaired and passes state inspections, it may receive a rebuilt title. This indicates the car is now legally roadworthy. A salvage title means the vehicle is still considered damaged and unsafe to drive, while a rebuilt title signals it has been restored to a drivable condition. Knowing the difference is key when bidding on insurance auction cars, as it affects resale value, insurance, and long-term reliability.

Can You Drive a Salvage Vehicle Legally?

Yes, but only if the vehicle has been properly repaired and inspected. A car with a salvage title alone cannot typically be driven on public roads. After repairs, obtaining a rebuilt title is required in most states. Even then, insurance coverage can be limited or more expensive, and buyers should always ensure all paperwork is complete before using the vehicle.

Where Can You Buy Insurance/Salvage Cars?

Buying insurance or salvage cars can save you thousands compared to retail prices, but it requires knowing where to look. From major auctions to specialized brokers, there are multiple avenues for budget-conscious buyers to access these vehicles safely.

Insurance Auto Auctions (IAAI, Copart, etc.)

Insurance auto auctions like IAAI (Insurance Auto Auctions) and Copart are the most common sources for salvage and insurance vehicles. These platforms list thousands of cars daily, including collision, theft recovery, flood-damaged, and repossessed vehicles. Buyers can bid online or in person, often paying much less than retail. However, some auctions require a dealer license, which limits direct access for individual buyers.

BidNDrive: Buying Through a Broker Without a Dealer License

For buyers without a dealer license, BidNDrive acts as a broker, giving access to insurance auctions safely. They handle bidding, paperwork, and shipping, making it easier for first-time or budget-conscious buyers to purchase vehicles legally. This service ensures you can get a salvage or insurance car without the hassle of dealing with complex auction rules yourself.

Buying Directly From Insurance Companies (Rare, But Possible)

Occasionally, insurance companies sell vehicles directly to the public. While this is less common, it can offer an opportunity to get a car at auction prices without intermediary fees. These sales often require contacting the insurance company directly and may involve local pick-up rather than nationwide shipping.

Local Impound & Tow Auctions

Local impound lots or tow auctions sometimes sell insurance or repossessed vehicles. These auctions can be a hidden gem for budget buyers looking for affordable options close to home. Cars may include minor accident vehicles, abandoned cars, or older models that insurance companies wrote off. Inspecting the vehicle carefully is crucial, as there is less information about history and condition compared to major online auctions.

How to Buy a Car From Insurance Companies (Step-By-Step)

Buying a car from an insurance company can seem complicated, but following a clear process helps budget-conscious buyers get the best deal. From registering on an auction platform to receiving your car, each step matters for a safe and cost-effective purchase.

Register on an Auction Platform

The first step is creating an account on a reputable insurance auto auction platform like Copart or IAA. Some platforms require a dealer license, so if you don’t have one, using a broker like BidNDrive is a practical solution. Registration typically involves providing ID and agreeing to auction rules. Once registered, you can browse listings and place bids on vehicles that meet your needs.

Set Your Budget (car price + fees + transport + repairs)

Before bidding, calculate your total budget. Include the auction price, auction fees, transportation costs, and potential repair expenses. For example, if a car is listed for $3,500, you may need to add $500–$1,000 for fees and shipping, plus extra if repairs are required. Setting a firm budget helps prevent overspending and ensures you’re prepared for the full cost of ownership.

Searching & Filtering for the Right Vehicle

Use filters to find cars that match your criteria, such as make, model, year, title type (salvage/clean), and damage type. Pay attention to vehicle history reports, photos, and any notes on condition. Filtering effectively saves time and increases the chance of finding a car that meets both your needs and budget.

Bidding Strategies (how to win without overpaying)

Successful bidding requires patience and strategy. Set a maximum bid based on your budget and stick to it. Monitor active auctions, watch for last-minute bidding wars, and avoid getting caught in emotional overspending. Sometimes bidding just under the maximum or waiting until the last few seconds increases your chances of winning at a fair price.

Payment & Documentation (what happens after winning)

After winning, you’ll need to pay the auction fees and car price within the platform’s timeline. The auction provides necessary documents, such as the title, bill of sale, and release forms. Ensure all paperwork is accurate and keep copies for your records. This step is critical for registering the vehicle and securing insurance.

Pickup, Shipping, and Delivery Options

Once payment and documentation are complete, arrange pickup or shipping. Some buyers handle transport themselves if local, while others hire transport companies for longer distances. Platforms like BidNDrive can manage shipping and delivery, making it easier for first-time buyers to receive their car safely and efficiently.

What to Look for When Buying a Damaged Car

Buying a damaged car from an insurance auction can save money, but it requires careful evaluation. Knowing what to inspect and how to estimate costs helps you avoid surprises and get a reliable vehicle for your budget.

Prioritize Cosmetic Damage (Cheapest + Easiest Repairs)

Start by looking at cosmetic issues such as scratches, dents, or minor bumper damage. These are usually inexpensive to fix compared to structural or engine problems. Cars with primarily cosmetic damage can often be restored to a great condition without breaking your budget, making them ideal for first-time salvage buyers.

Verify if the Car Is Drivable

Before bidding, check whether the car is drivable or requires towing. A drivable vehicle reduces additional costs and hassle. Non-running cars can be bought cheaply but may require expensive repairs, so assess whether you’re willing to invest time and money into getting it back on the road.

Know the Real Repair Cost (Parts + Labor)

Estimate the total repair costs, including both parts and labor. Online resources, local mechanics, or forums can help you determine what repairs will cost. For example, replacing a headlight or bumper is cheap, but engine, transmission, or frame repairs can quickly exceed your budget if not planned for.

Know the Model (Some Brands = Expensive Repairs)

Some brands have higher maintenance and parts costs, even for minor repairs. Luxury or European cars often require expensive components, while domestic or Japanese models tend to be more budget-friendly. Research the model’s reliability and typical repair costs before bidding to avoid overspending.

Negotiating on Price (When Buying Locally)

If buying from a local insurance or impound sale, don’t hesitate to negotiate the price. Highlight cosmetic damage, missing parts, or minor mechanical issues to justify a lower offer. Even small reductions can make a big difference for buyers on a tight budget.

Evaluating Vehicle Conditions

When buying a car from an insurance auction, carefully evaluating its condition is crucial. A thorough inspection helps budget-conscious buyers avoid costly surprises and make informed bidding decisions.

Inspection Tips (What Photos Reveal)

Even if you can’t see the car in person, auction photos reveal a lot. Look closely at body panels, paint mismatches, and alignment of doors and bumpers—these can indicate previous accidents or frame damage. Check the engine bay for leaks, missing components, or signs of poor maintenance. Interior photos can show wear on seats, dashboard cracks, or water damage. Learning to read photos effectively saves time and money.

Common Issues to Watch For (Frame, Airbags, Rust, Floods)

- Frame Damage: Look for misaligned panels, uneven gaps, or bent chassis; repairing structural damage is expensive.

- Airbags: Deployed or missing airbags mean additional repair costs. Confirm their status in photos or auction notes.

- Rust: Check wheel wells, door sills, and undercarriage; rust can spread and become costly to fix.

- Flood Damage: Signs include water stains, mildew smells, or corroded metal and electronics. Flooded cars may have hidden electrical or engine issues.

Importance of Vehicle History Reports (Carfax, AutoCheck, VIN Decoding)

A vehicle history report is essential for understanding past incidents. Services like Carfax or AutoCheck provide info on accidents, title status, odometer readings, and service history. Decoding the VIN can reveal manufacturer recalls, insurance write-offs, and original specifications. Combining history reports with inspection photos helps buyers make a confident decision and avoid hidden risks.

Pros and Cons of Buying a Salvage or Insurance Car

Buying a salvage or insurance car can be a smart way to save money, but it comes with both advantages and risks. Understanding the pros and cons helps budget-conscious buyers make informed decisions before bidding at an auction.

Pros

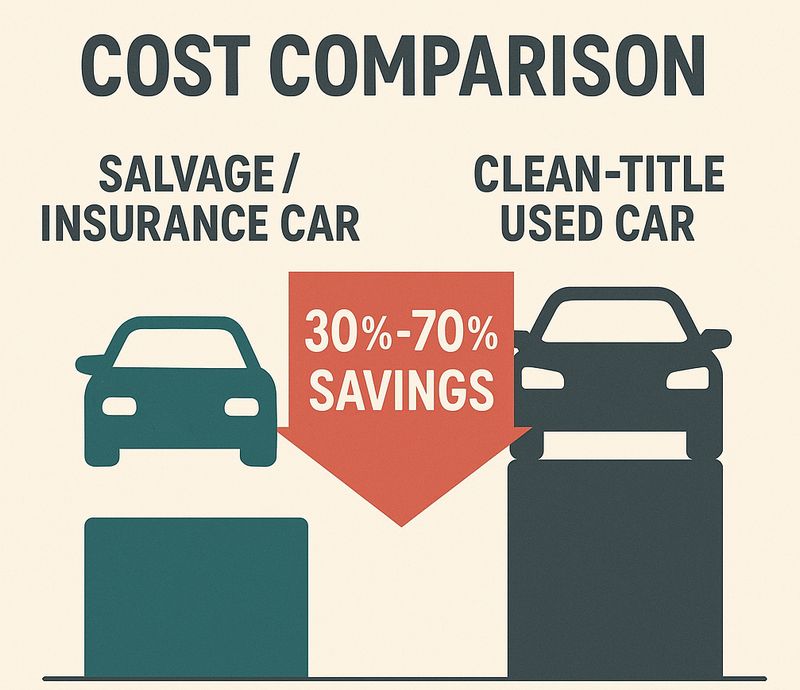

Major Cost Savings (Often 30–70% Below Market Value)

One of the biggest benefits is the significant price reduction. Salvage and insurance cars typically sell for 30–70% less than comparable clean-title vehicles. For buyers on a tight budget, this makes cars that would otherwise be unaffordable accessible. Even accounting for repairs, the total cost can still be far lower than buying a traditional used car.

Opportunity to Rebuild & Resell

For mechanically inclined buyers, salvage cars offer a chance to rebuild and even resell for profit. Fixing cosmetic or minor mechanical issues can turn a low-cost purchase into a functional, roadworthy vehicle. Some buyers even restore vehicles for personal use or flip them to recoup their investment, making this a flexible option for those willing to put in some work.

Cons

Banks May Not Finance

Financing a salvage vehicle can be challenging. Many banks and lenders avoid providing loans for salvage-title cars due to the risk involved. Buyers often need to pay cash or find specialized lenders, which may limit options for those relying on traditional financing.

Resale Value Differences

Even after repairs, salvage or rebuilt-title cars typically have lower resale value compared to clean-title vehicles. Buyers should be aware that if they plan to sell the car later, they may not recoup as much as they would with a standard used car, which can affect long-term investment decisions.

Can I Insure a Salvage or Rebuilt Vehicle?

Many buyers wonder if a salvage or rebuilt vehicle can be insured. The answer is yes, but it comes with restrictions and considerations. Understanding the process helps budget-conscious buyers plan for insurance costs and coverage.

When Insurance Is Possible (Rebuilt Title)

Insurance is generally possible for vehicles with a rebuilt title. After a salvage car has been repaired and passes state inspections, it can be legally driven and insured. Standard liability coverage is usually available, and some insurers may offer comprehensive and collision coverage, though often at a higher premium.

Why Full Coverage Is Harder to Get

Full coverage (comprehensive and collision) is harder to obtain for rebuilt or salvage vehicles because insurers consider them higher risk. Even after repairs, there may be hidden damage, reduced structural integrity, or prior accident history that affects the car’s value and claim potential. Some insurance companies simply refuse full coverage on these vehicles.

How to Increase Chances of Approval (Inspection, Receipts)

To improve your chances of getting insured, provide thorough documentation:

- Inspection reports confirming the car is roadworthy.

- Repair receipts showing quality parts and professional work.

- Vehicle history reports to verify the car’s current condition.

Are you interested in buying a vehicle from Online Auto Auctions?

With this being said – you can still export vehicles and save up a few thousand dollars with Bidndrive. We have an inventory of over 150k plus vehicles with titles you can export for you to choose from. Once you have placed your bid and won the auction a Bill of Sale document is then emailed to you as proof of purchase – after full payments have been made.

To gain access and get started on your purchase, sign up for free.

Further Reading:

Why Do Used Cars Go to Auction? Process & Benefits Explained

Salvage Title: What Does It Mean and Should You Buy One?

Should You Buy a Salvage Car? Pros, Cons, and Expert Tips

How to Check a Car Title by VIN

Frequently Asked Questions

- Which insurance company is best for cars?

- What is the best way to buy car insurance?