Cybersecurity and data protection have become critical responsibilities for modern auto dealerships. The FTC Safeguards Rule requires dealers to protect customer financial information, reduce security risks, and maintain written compliance programs. This guide explains the rule in simple terms, helping dealership owners and managers understand the requirements, avoid costly mistakes, strengthen data security, and build customer trust.

What Is the FTC Safeguards Rule?

The FTC Safeguards Rule is a federal regulation that requires businesses handling consumer financial information to protect that data from unauthorized access, theft, or misuse. For auto dealerships, the rule is especially important because dealers regularly collect sensitive customer information during vehicle sales, financing, leasing, and credit applications.

Many dealership owners focus on selling cars, managing inventory, and serving customers. However, customer data has become one of the most valuable assets inside a dealership. The Safeguards Rule helps businesses create procedures that reduce cybersecurity risks and protect both customers and the dealership itself.

Purpose of the FTC Safeguards Rule

The primary purpose of the FTC Safeguards Rule is to protect customer information. The rule requires businesses to develop, implement, and maintain a written information security program that matches the size and complexity of the company.

The goal is not simply to satisfy regulators. The rule aims to prevent situations such as:

- stolen customer identities;

- unauthorized access to financing records;

- ransomware attacks;

- leaked Social Security numbers;

- stolen credit applications;

- compromised bank account information.

For example, a small used car dealership may keep financing documents on an office computer. If that computer becomes infected with malware, customer information could be exposed. The Safeguards Rule requires businesses to identify these risks and reduce them before a problem occurs.

The rule focuses on prevention rather than reacting after a security breach happens.

The Gramm-Leach-Bliley Act (GLBA) Connection

The FTC Safeguards Rule originates from the Gramm-Leach-Bliley Act, commonly called the GLBA. This federal law was passed to protect consumers' financial information and to establish privacy requirements for businesses that handle financial data.

Under the GLBA, companies that provide financial products or services must protect customer information. Because many dealerships arrange financing, process credit applications, or offer payment plans, they often qualify as financial institutions under the law.

Many dealers are surprised to learn this. A dealership may think of itself as a vehicle retailer, but the government may view it as a financial institution because it helps customers obtain financing.

For example, if a dealership:

- submits credit applications;

- arranges vehicle loans;

- collects income information;

- verifies employment;

- handles financing contracts;

it may fall under the Safeguards Rule requirements.

The FTC enforces these requirements to ensure businesses protect sensitive customer data.

Why the Rule Applies to Auto Dealerships

Modern dealerships collect a large amount of personal and financial information. During a single vehicle sale, a dealer may receive:

- driver's licenses;

- Social Security numbers;

- bank statements;

- credit reports;

- employment records;

- income documentation;

- insurance information;

- payment details.

This information can be valuable to cybercriminals. A stolen customer file may contain enough information to commit identity theft or financial fraud.

Consider a small independent dealership that stores scanned driver's licenses and credit applications on an office computer without passwords or encryption. If an employee clicks on a phishing email, the dealership may experience a data breach affecting dozens or even hundreds of customers.

Because dealerships handle sensitive financial information, the FTC considers them responsible for protecting that data.

The Safeguards Rule recognizes that dealerships are no longer simply car lots. They are businesses that manage significant amounts of consumer financial information.

Which Dealerships Must Comply?

Many automotive businesses fall under the Safeguards Rule. Compliance is not limited to large franchise dealers.

Businesses that may need to comply include:

- franchised dealerships;

- independent used car dealers;

- Buy Here Pay Here dealers;

- leasing companies;

- finance companies;

- vehicle brokers;

- auction dealers;

- dealerships arranging customer financing.

Size does not determine whether the rule applies. A small dealership with only a few employees may still have compliance obligations if it handles customer financial information.

For example, a small used car dealer that helps customers obtain loans from local banks may be subject to the rule even if it only sells a few vehicles each month.

Many smaller dealerships face budget limitations and may not have dedicated IT staff. The Safeguards Rule recognizes that businesses differ in size, but it still expects reasonable security measures based on the risks involved.

Key Updates to the Safeguards Rule

The FTC updated the Safeguards Rule to address modern cybersecurity threats. The newer requirements are more detailed than earlier versions and place greater responsibility on businesses.

Important updates include:

- appointing a Qualified Individual to oversee security;

- conducting formal risk assessments;

- implementing multi-factor authentication;

- monitoring and testing security controls;

- encrypting sensitive information;

- developing incident response plans;

- overseeing service providers;

- reporting security findings to management.

These changes reflect the reality that cyberattacks have become more common and more expensive.

For example, a dealership may have previously relied on antivirus software alone. Under the updated rule, that is usually not enough. Businesses are expected to evaluate risks, train employees, document procedures, and continuously improve their security programs.

The updated Safeguards Rule does not require every dealership to build a large IT department. However, it does require dealerships to take customer information seriously and implement reasonable safeguards that match their operations.

Why the FTC Safeguards Rule Matters for Auto Dealers

Many dealerships think of cybersecurity as a problem for large corporations, banks, or technology companies. In reality, auto dealerships have become attractive targets for cybercriminals because they collect large amounts of valuable customer information.

The FTC Safeguards Rule matters because a data breach can affect both customers and the dealership itself. Lost data, financial losses, legal expenses, and damaged customer trust can create serious problems for businesses of any size. Even a small dealership with only a few employees can become a target.

Growing Cybersecurity Threats in the Automotive Industry

Cyberattacks against automotive businesses have increased significantly in recent years. Dealerships use digital systems for inventory management, financing, customer records, marketing, accounting, and communication. Every connected system creates a potential security risk.

Common threats include:

- phishing emails;

- ransomware attacks;

- stolen passwords;

- malware infections;

- unauthorized system access;

- fake vendor invoices;

- data theft;

- social engineering scams.

For example, an employee may receive an email that appears to come from a finance company or software provider. After clicking a link, malware may gain access to customer files stored on the dealership network.

Small dealerships can be especially vulnerable because they often operate with limited IT resources. Some businesses still use outdated computers, shared passwords, or unsecured wireless networks.

Cybercriminals do not only target large dealerships. Smaller businesses may actually become easier targets because their security systems are less advanced.

Types of Customer Information Dealerships Collect

Many people do not realize how much sensitive information dealerships collect during a vehicle transaction. A single deal file may contain enough information to commit identity theft or financial fraud.

Dealerships commonly collect:

- full names;

- home addresses;

- phone numbers;

- email addresses;

- driver's licenses;

- Social Security numbers;

- employment information;

- income records;

- bank account information;

- credit applications;

- insurance documents;

- financing agreements.

Buy Here Pay Here dealers often collect even more financial information because they handle their own financing programs.

For example, a customer applying for a vehicle loan may provide tax documents, pay stubs, bank statements, and personal identification. If this information is not properly protected, it may be exposed during a security incident.

Both paper files and electronic records must be protected under the Safeguards Rule.

Financial Risks of Data Breaches

A data breach can become extremely expensive for a dealership. The cost goes far beyond repairing computer systems.

Potential financial consequences include:

- legal expenses;

- forensic investigations;

- customer notifications;

- credit monitoring services;

- system recovery costs;

- business interruption;

- regulatory penalties;

- lawsuits;

- lost sales;

- increased insurance costs.

Consider a small dealership that experiences a ransomware attack. Employees may lose access to customer records, financing systems, and sales documents. The dealership may be unable to complete transactions for several days while systems are restored.

Even if the business survives the incident, recovery costs can be substantial.

For dealerships operating on small profit margins, a major security incident can become a serious financial burden.

Customer Trust and Reputation Protection

Trust is extremely important in the automotive business. Customers provide sensitive information because they believe the dealership will protect it.

A security incident can damage that trust very quickly.

If customers learn that their personal information was exposed, they may:

- avoid future purchases;

- leave negative reviews;

- share their experience online;

- file complaints;

- recommend competitors;

- lose confidence in the dealership.

For example, a family purchasing their first vehicle may submit credit applications, income documents, and identification records. If those documents are later compromised, the customer may never return to that dealership.

Small businesses often depend heavily on local reputation and referrals. A damaged reputation can affect future sales long after the security incident is resolved.

Strong security practices help demonstrate that the dealership takes customer information seriously.

Regulatory Expectations for Modern Dealerships

Government agencies increasingly expect dealerships to protect customer information using reasonable security practices. The FTC Safeguards Rule reflects these expectations.

Regulators now expect businesses to:

- identify security risks;

- document security procedures;

- train employees;

- monitor systems;

- control access to data;

- manage vendors;

- respond to security incidents;

- review security programs regularly.

Many dealerships still rely on practices that worked years ago, such as shared passwords, unlocked filing cabinets, or employee access to all customer records. These approaches may no longer be sufficient.

For example, a dealership with ten employees does not necessarily need a large cybersecurity department. However, it should know:

- where customer information is stored;

- who can access it;

- how data is protected;

- how employees are trained;

- what happens if a security incident occurs.

The FTC recognizes that businesses vary in size and resources. The expectation is not perfection. The expectation is reasonable protection based on the risks involved.

Buy Inventory Securely Through Trusted Auction Channels

Modern dealerships manage sensitive customer information every day. BidNDrive helps dealers purchase vehicles through a secure and transparent auction platform while providing access to verified inventory and reliable transaction processes.

- ✅ Access to dealer-only auction inventory

- ✅ Transparent vehicle purchasing process

- ✅ Free vehicle history reports with active deposit

- ✅ Support for independent and franchised dealers

Which Auto Businesses Must Follow the FTC Safeguards Rule?

Many automotive businesses assume that the FTC Safeguards Rule only applies to large franchised dealerships. In reality, the rule covers a much wider range of businesses that handle customer financial information.

If a business helps arrange financing, collects credit information, processes payments, or stores sensitive customer records, it may fall under the rule. The size of the company is less important than the type of information it collects and how that information is used.

Understanding whether your business must comply is the first step toward building an effective information security program.

Franchised Auto Dealerships

Franchised dealerships are among the businesses most clearly covered by the FTC Safeguards Rule. New vehicle dealerships regularly collect financial and personal information during the sales and financing process.

These dealerships often handle:

- credit applications;

- financing agreements;

- lease contracts;

- trade-in documentation;

- driver's licenses;

- insurance information;

- employment verification;

- income records.

Because franchised dealerships work closely with lenders, manufacturers, and finance companies, they process large amounts of customer data every day.

A dealership selling dozens or hundreds of vehicles each month may have thousands of customer records stored in its systems. Protecting this information is one of the primary reasons the Safeguards Rule applies.

Many large dealerships already have IT departments and compliance teams, but they still must maintain documented security programs and regularly evaluate risks.

Independent Used Car Dealers

Independent used car dealerships are often surprised to learn that they may also be covered by the rule.

Even a small dealer with only a few employees may collect:

- financing applications;

- copies of driver's licenses;

- Social Security numbers;

- income documents;

- bank information;

- customer payment records.

For example, an independent dealer may help a customer obtain financing through a local bank or finance company. Once the dealership collects and transmits financial information, compliance obligations may apply.

Small dealers often face additional challenges because they may not have dedicated cybersecurity staff. Customer information may be stored on office computers, external hard drives, email accounts, or cloud storage systems.

The FTC expects businesses to implement reasonable safeguards based on their size and risk level. A small dealership does not need the same resources as a large dealer group, but it still needs security controls.

Buy Here Pay Here (BHPH) Dealers

Buy Here Pay Here dealerships usually have significant compliance responsibilities because they directly finance customers.

BHPH dealers often collect extensive financial information, including:

- credit applications;

- employment records;

- income verification;

- banking information;

- payment histories;

- references;

- identification documents.

Since these dealerships act as both seller and lender, they handle sensitive financial information throughout the entire customer relationship.

For example, a BHPH dealership may manage customer payment records for several years after the vehicle sale. This means customer information remains stored in company systems long after the transaction is complete.

Because of this increased exposure, BHPH dealers often face higher data security risks and must pay close attention to information protection.

Auto Finance Companies

Auto finance companies clearly fall within the scope of the Safeguards Rule because their primary business involves financial services.

These companies routinely manage:

- loan applications;

- credit reports;

- payment information;

- account records;

- customer financial data;

- collection information.

Finance companies often maintain large databases containing highly sensitive information. A security breach affecting a finance company can expose thousands of customer records.

Because of the amount of financial information involved, finance companies typically maintain more extensive cybersecurity programs, risk assessments, and monitoring systems.

Their compliance responsibilities are often broader than those of smaller dealerships.

Leasing Companies

Vehicle leasing companies may also be subject to the Safeguards Rule because leasing transactions involve financial services and customer financial information.

Leasing companies frequently collect:

- credit information;

- income documentation;

- payment information;

- insurance records;

- employment verification;

- identification documents.

Customers often enter lease agreements for several years, meaning companies may store sensitive information for extended periods.

For example, a leasing company may maintain customer records throughout the lease term and beyond for legal, tax, or business purposes.

As a result, proper data security becomes an important part of their operations.

Auction Dealers and Vehicle Brokers

Auction dealers, vehicle brokers, and automotive intermediaries may also fall under the Safeguards Rule depending on their business activities.

These businesses often:

- assist with financing;

- collect customer information;

- process deposits;

- arrange vehicle purchases;

- communicate with lenders;

- handle transaction documents.

For example, an auction broker helping customers purchase vehicles may collect copies of driver's licenses, financing information, wire instructions, or identification documents.

Vehicle brokers who only connect buyers and sellers without handling financial information may face fewer compliance obligations. However, once customer financial data is collected or transmitted, Safeguards Rule requirements may apply.

Businesses involved in online vehicle transactions should carefully evaluate the information they collect and how it is stored.

Exemptions and Special Cases

Not every automotive business automatically falls under the FTC Safeguards Rule. Certain businesses may qualify for exemptions depending on their activities.

For example, a dealership that accepts only cash payments and never arranges financing may have different obligations than a dealer that regularly submits credit applications.

Some factors that may affect coverage include:

- whether financing is offered;

- whether customer financial information is collected;

- whether credit applications are processed;

- whether payment information is stored;

- the type of business operations.

However, many dealerships underestimate their exposure. A business may believe it is exempt because it does not provide direct financing, while still collecting and transmitting customer financial information to lenders.

For example, a small used car dealer that sends customer credit applications to outside banks may still be subject to the rule.

Because each business operates differently, dealership owners should carefully evaluate their activities and seek professional guidance if necessary.

Understanding the FTC Safeguards Rule Requirements

The FTC Safeguards Rule requires covered dealerships to create a clear system for protecting customer information. This does not mean every dealer needs a large cybersecurity department. It means the dealership must understand what customer data it collects, where that data is stored, who can access it, and how it is protected.

For small and mid-sized dealers, compliance can feel overwhelming at first. The best approach is to break the rule into practical steps: assign responsibility, assess risks, write policies, train employees, control access, monitor systems, manage vendors, and prepare for security incidents.

Overview of the Eight Core Compliance Requirements

The Safeguards Rule includes several important requirements that work together to protect customer information. For dealerships, these requirements should be treated as a practical security framework rather than a one-time paperwork task.

Key compliance areas include:

- appointing a Qualified Individual to oversee the security program;

- conducting a written risk assessment;

- creating and maintaining a written information security program;

- implementing safeguards to control identified risks;

- training employees;

- monitoring and testing security controls;

- overseeing third-party service providers;

- preparing an incident response plan;

- reporting security information to ownership or management.

Some guides describe these as eight core requirements, while the FTC explains the rule through several required program elements. The main point is the same: dealerships must build a security program that is written, active, and based on real risks inside the business.

For example, a small independent dealer may not need the same tools as a large dealer group. But it still needs to protect credit applications, scanned IDs, customer financing records, and payment information from unauthorized access.

Building a Written Information Security Program (WISP)

A Written Information Security Program, often called a WISP, is the main document that explains how the dealership protects customer information.

A WISP should describe:

- what customer information the dealership collects;

- where that information is stored;

- who has access to it;

- what safeguards protect it;

- how employees are trained;

- how vendors are reviewed;

- how incidents are handled;

- how the program is updated over time.

The WISP should not be a generic file that sits in a folder and is never used. It should reflect how the dealership actually operates.

For example, if a dealership stores credit applications in a cloud-based dealer management system, the WISP should mention that system and explain who can access it. If paper deal jackets are kept in filing cabinets, the WISP should explain how those cabinets are secured and who is responsible for them.

A simple but accurate WISP is often more useful than a long template that does not match the business.

Risk-Based Compliance Approach

The Safeguards Rule uses a risk-based approach. This means dealerships should focus on the risks that actually apply to their business.

A small used car dealer with five employees may have different risks than a large franchised dealer with multiple locations. A Buy Here Pay Here dealer may face additional risks because it stores payment records and customer financial data for a longer period.

A risk-based approach asks practical questions:

- What customer information do we collect?

- Where do we store it?

- Who can access it?

- How could it be lost, stolen, or misused?

- What systems are most vulnerable?

- What would happen if we had a data breach?

- What safeguards are reasonable for our size and operations?

For example, if employees share one login to access customer records, that is a clear risk. If old laptops contain customer files and are not encrypted, that is another risk. If former employees still have access to dealership email or software, that risk should be addressed quickly.

The goal is not perfection. The goal is to identify real threats and take reasonable steps to reduce them.

Documentation and Recordkeeping Requirements

Documentation is a major part of compliance. If a dealership cannot show what it has done, it may be difficult to prove that it has a real security program.

Important records may include:

- written information security program;

- written risk assessments;

- employee training records;

- vendor review records;

- access control policies;

- incident response plan;

- security testing results;

- management reports;

- records of program updates.

For example, if a dealership trains employees on phishing emails, it should keep a record of when the training happened and who completed it. If the dealership reviews a software provider, it should keep notes or documents showing that review.

Good documentation also helps the business operate better. When a new employee is hired, written procedures make onboarding easier. When a vendor changes, records help management understand what data the vendor can access. If a security incident occurs, documentation helps the dealership respond faster.

For small dealerships with limited staff, documentation does not need to be complicated. A clear folder with updated policies, training records, vendor information, and risk assessments is a strong starting point.

Appointing a Qualified Individual

One of the key requirements of the FTC Safeguards Rule is appointing a Qualified Individual to oversee the dealership’s information security program. This person is responsible for making sure the program is not just written on paper, but actually used in daily operations.

For auto dealers, this role is important because customer information moves through many parts of the business: sales, finance, accounting, service, management, vendors, and software systems. Without one responsible person or team, security tasks can be missed.

Who Can Serve as the Qualified Individual?

The Qualified Individual does not have to hold a specific job title. The FTC does not require this person to be called a Chief Information Security Officer or to have a particular certification.

The person may be:

- an owner;

- a general manager;

- an office manager;

- an IT manager;

- a compliance manager;

- an outside cybersecurity consultant;

- a managed IT service provider.

What matters most is that the person has the ability, authority, and knowledge needed to oversee the information security program.

For a large dealership group, the Qualified Individual may be a dedicated cybersecurity professional. For a small used car dealer, it may be the owner working with an outside IT provider.

For example, a three-person independent dealership may not have an internal IT department. In that case, the owner may appoint an outside security consultant to help manage risk assessments, employee training, access controls, and incident planning.

The role should be clearly documented so employees know who is responsible for security decisions.

Internal vs External Security Leadership

Dealerships can appoint someone inside the business or hire an outside expert to serve or support the Qualified Individual role. Each approach has advantages and challenges.

An internal person understands the dealership’s daily operations. They know how sales staff collect documents, how financing files are stored, which vendors are used, and where common workflow problems occur.

However, an internal employee may not have enough technical knowledge to manage cybersecurity risks alone.

An external provider may bring stronger technical experience. They can help with:

- risk assessments;

- network security;

- employee training;

- written policies;

- incident response planning;

- vendor security reviews;

- security testing.

The drawback is that an outside provider may not fully understand the dealership’s actual workflow unless management gives clear information.

For many small and mid-sized dealerships, the best solution is a combination. An internal manager coordinates the program, while an outside IT or cybersecurity provider supports technical work.

Responsibilities of the Qualified Individual

The Qualified Individual is responsible for overseeing the dealership’s information security program. This does not mean they must do every task alone, but they must make sure the required work is completed.

Key responsibilities may include:

- overseeing the Written Information Security Program;

- coordinating risk assessments;

- reviewing security risks;

- helping select safeguards;

- monitoring employee training;

- reviewing vendor security practices;

- checking access controls;

- helping prepare the incident response plan;

- monitoring updates to the security program;

- reporting to ownership or management.

For example, if employees are storing customer credit applications in personal email accounts, the Qualified Individual should identify that risk and recommend a safer process.

If a former employee still has access to dealership software, the Qualified Individual should make sure access is removed quickly.

The role is practical. It connects written compliance requirements with real dealership behavior.

Reporting Requirements to Ownership and Management

The Safeguards Rule expects the Qualified Individual to report regularly to senior management or ownership. This helps ensure that security is treated as a business issue, not just an IT problem.

Reports should explain:

- current security risks;

- results of risk assessments;

- status of safeguards;

- employee training progress;

- vendor issues;

- security incidents;

- needed improvements;

- budget or resource needs.

For a small dealership, this report does not need to be overly complicated. A short written summary may be enough if it clearly shows what has been reviewed and what needs attention.

For example, a quarterly report might state that all employees completed phishing training, one former employee account was removed, the dealership updated password rules, and a vendor review is still pending.

The purpose of reporting is accountability. Owners and managers need to know whether customer information is being protected and whether the dealership is meeting its obligations.

Ongoing Oversight and Accountability

Appointing a Qualified Individual is not a one-time task. The person must continue overseeing the security program as the dealership changes.

Security risks can change when:

- new software is added;

- employees are hired or leave;

- vendors change;

- remote access is introduced;

- new financing processes are used;

- customer records move to cloud storage;

- cyber threats increase.

For example, a dealership may start using a new customer relationship management system. The Qualified Individual should evaluate who can access the system, what customer data is stored there, and whether vendor protections are adequate.

Accountability also matters. If no one checks whether security rules are followed, employees may return to unsafe habits like sharing passwords, emailing sensitive documents, or leaving customer files on desks.

The Qualified Individual should help keep the program active, updated, and realistic.

Conducting a Comprehensive Risk Assessment

A risk assessment is one of the most important parts of FTC Safeguards Rule compliance. It helps a dealership understand where customer information is stored, how it could be exposed, and what steps are needed to reduce risk.

For many small dealerships, this process does not have to be complicated. The main goal is to look honestly at daily operations. Where are credit applications kept? Who can access customer files? Are passwords shared? Are documents sent by unsecured email? These simple questions can reveal serious security gaps.

Identifying Sensitive Customer Information

The first step in a risk assessment is identifying what sensitive information the dealership collects and stores. Many dealers underestimate how much customer data moves through the business during a normal vehicle sale.

Sensitive customer information may include:

- credit applications;

- Social Security numbers;

- driver’s licenses;

- home addresses;

- phone numbers;

- email addresses;

- employment records;

- income documents;

- bank statements;

- payment information;

- loan and lease documents;

- insurance records;

- trade-in documents.

For example, a used car dealer may collect a customer’s driver’s license for a test drive, then collect income information for financing, then store a signed purchase agreement after the sale. Each of these records may contain private data.

The dealership should list what information it collects, where it is stored, how long it is kept, and who can access it.

Both paper records and digital records matter. A locked filing cabinet and a secure cloud system may both be part of the same risk assessment.

Evaluating Internal Security Risks

Internal risks come from the dealership’s own systems, processes, and habits. These risks are often easier to fix once they are identified.

Common internal risks include:

- shared employee passwords;

- unlocked file cabinets;

- old computers without updates;

- customer files stored on desktops;

- unsecured Wi-Fi networks;

- weak email security;

- lack of employee access controls;

- missing backups;

- outdated software;

- poor document disposal practices.

For example, if every salesperson uses the same login to access financing records, the dealership may not know who viewed or changed customer information. This creates both security and accountability problems.

Another common issue is storing scanned customer documents on a shared office computer. If that computer is not protected, customer information may be exposed.

A strong risk assessment should review how the dealership actually works day to day, not just what the written policy says.

Assessing External Threats and Cyberattacks

External threats come from outside the dealership. These may include hackers, scammers, malware, ransomware groups, phishing campaigns, and criminals trying to steal customer data.

Dealerships are attractive targets because they collect financial information and often work with lenders, vendors, auctions, transport companies, and software providers.

External threats may include:

- phishing emails that look like lender messages;

- fake invoices from vendors;

- ransomware attacks;

- stolen login credentials;

- malware from unsafe downloads;

- attacks on cloud software;

- unauthorized remote access;

- compromised vendor accounts.

For example, an employee may receive an email that appears to come from a finance company asking them to open an attachment. If the attachment contains malware, the dealership’s customer files could be at risk.

The risk assessment should evaluate how the dealership protects itself from these threats. This may include email filtering, multi-factor authentication, antivirus tools, secure backups, employee training, and vendor controls.

Evaluating Employee-Related Risks

Employees play a major role in dealership security. Even strong software cannot protect customer information if employees are not trained or if access is poorly managed.

Employee-related risks may include:

- lack of cybersecurity training;

- sharing passwords;

- clicking phishing links;

- sending sensitive documents by unsecured email;

- leaving customer files on desks;

- using personal devices for work;

- accessing information they do not need;

- failing to report suspicious activity;

- former employees keeping system access.

For example, a former salesperson may still have access to the dealership’s CRM or email account after leaving the company. If that account is later misused, customer information could be exposed.

The dealership should review employee access regularly. Each employee should only have access to the information needed for their job.

Training is also important. Employees should know how to recognize phishing emails, protect documents, use strong passwords, and report security concerns quickly.

Prioritizing and Documenting Findings

After identifying risks, the dealership should prioritize them. Not every issue has the same level of urgency.

High-risk issues should be addressed first. These may include:

- customer data stored without passwords;

- no multi-factor authentication;

- former employees with active access;

- unencrypted sensitive files;

- unsecured remote access;

- unresolved malware infections;

- lack of backups;

- flood of phishing attempts;

- missing incident response procedures.

Lower-risk issues can still matter, but dealerships with limited budgets need to focus first on problems that could cause the most harm.

For example, replacing all office computers may be expensive and take time. But removing former employee access and enabling multi-factor authentication may be faster and reduce major risk quickly.

Documentation is essential. The dealership should record:

- identified risks;

- risk level;

- affected systems or records;

- recommended fixes;

- responsible person;

- target completion date;

- completed actions.

This documentation shows that the dealership is actively managing risk instead of ignoring it.

Updating Risk Assessments Over Time

A risk assessment is not a one-time project. Dealership operations change, technology changes, and cyber threats change.

The dealership should update its risk assessment when major changes happen, such as:

- adding new software;

- changing finance providers;

- hiring or terminating employees;

- moving records to cloud storage;

- adding remote access;

- expanding to another location;

- changing payment systems;

- experiencing a security incident.

At minimum, dealerships should review their risk assessment regularly and update it when new risks appear.

For example, a dealer may start using a new online credit application tool. Before using it fully, the Qualified Individual should review what customer information the tool collects, where the data is stored, and how the vendor protects it.

Regular updates help keep the information security program realistic and useful.

Customer Information Covered by the Safeguards Rule

Many dealerships are surprised by how much customer information falls under the FTC Safeguards Rule. The rule does not only apply to loan applications or bank records. It covers a wide range of personal and financial information collected during vehicle sales, financing, leasing, and service transactions.

Understanding what information must be protected is essential for compliance. If a dealership does not know what data it has, it cannot properly secure it. Both paper documents and electronic records may contain sensitive information that requires protection.

Financial Information

Financial information is one of the primary categories covered by the Safeguards Rule. Dealerships often collect financial data to help customers obtain financing, verify their ability to pay, or complete transactions.

Financial information may include:

- credit scores;

- loan amounts;

- monthly income;

- down payment information;

- debt obligations;

- payment history;

- financing terms;

- account balances;

- financial statements.

For example, a customer applying for a vehicle loan may provide information about monthly income, housing expenses, and existing debts. This information helps lenders make credit decisions, but it also creates a responsibility to protect that data.

Unauthorized access to financial information can lead to fraud, identity theft, and financial losses for customers.

Credit Applications and Loan Documents

Credit applications contain some of the most sensitive information collected by dealerships. These documents often combine financial information with personal identification details.

Typical documents may include:

- credit applications;

- retail installment contracts;

- loan approvals;

- financing agreements;

- lender communications;

- credit reports;

- co-signer information;

- loan disclosures.

For example, a dealership finance office may collect a completed credit application and submit it to multiple lenders. Copies of these documents may be stored in paper files, dealer management systems, email accounts, or cloud storage.

Because these documents contain large amounts of sensitive information, they should only be accessible to authorized employees.

Improper handling of credit applications is one of the most common security risks in automotive businesses.

Driver’s Licenses and Government IDs

Dealerships frequently collect copies of driver's licenses and other government-issued identification documents. These records may be used during:

- test drives;

- financing applications;

- vehicle purchases;

- identity verification;

- insurance verification;

- title transfers.

A driver's license contains valuable personal information, including:

- full legal name;

- address;

- date of birth;

- license number;

- physical description;

- identification photographs.

For example, a salesperson may scan a customer's driver's license before a test drive. If those images are stored on an unsecured computer or shared folder, the dealership may create unnecessary security risks.

Government-issued identification should be protected just like financial records.

Social Security Numbers

Social Security numbers are among the most sensitive pieces of customer information a dealership may collect.

These numbers are commonly used during:

- credit applications;

- loan processing;

- identity verification;

- financing approvals.

Criminals often seek Social Security numbers because they can be used for identity theft, fraudulent loans, or financial fraud.

For example, a customer applying for financing may provide a Social Security number to multiple lenders through the dealership. If that information is exposed, the customer may face long-term financial consequences.

Access to Social Security numbers should be strictly limited. Employees who do not need this information to perform their jobs should not have access to it.

Encryption, secure storage, and proper disposal procedures are especially important when handling these records.

Bank Account and Payment Information

Many dealerships collect banking information to process payments, arrange automatic withdrawals, or verify customer accounts.

This information may include:

- bank account numbers;

- routing numbers;

- debit card information;

- payment authorization forms;

- electronic payment records;

- ACH information;

- account verification documents.

Buy Here Pay Here dealerships may collect this information to manage recurring payments. Other dealerships may use it for down payments, deposits, or financing transactions.

For example, a dealership that stores customer banking information in unsecured spreadsheets creates a significant security risk. If unauthorized access occurs, customers may experience financial losses.

Payment information should be stored securely and only retained as long as necessary.

Employment and Income Verification Records

Lenders often require proof of employment and income before approving vehicle financing. As a result, dealerships may collect documents that reveal significant personal information.

Examples include:

- pay stubs;

- tax returns;

- employer information;

- bank statements;

- income verification letters;

- self-employment records;

- retirement income documents.

A customer may provide several months of financial records during the financing process. These documents often contain account numbers, employer information, addresses, and income details.

Because these records contain both financial and personal information, they require strong protection.

Dealerships should review how these documents are collected, transmitted, stored, and eventually destroyed.

Digital Records and Electronic Communications

The Safeguards Rule applies to electronic records just as much as paper files. Modern dealerships often store customer information in multiple digital systems.

Examples include:

- customer relationship management systems;

- dealer management software;

- email accounts;

- cloud storage platforms;

- accounting systems;

- financing portals;

- scanned documents;

- text messages;

- online applications;

- digital contracts.

For example, an employee may email a customer's credit application to a lender. Another employee may store scanned documents in a shared network folder. A salesperson may receive customer information through text messages.

All of these records may contain protected customer information.

Electronic communications can create risks if they are not properly secured. Unencrypted emails, weak passwords, shared accounts, and unsecured cloud storage may expose customer information to unauthorized access.

Dealerships should understand where electronic information is stored, who can access it, how it is protected, and how long it is retained.

Technical Safeguards Required for Compliance

The FTC Safeguards Rule does not require dealerships to purchase the most expensive cybersecurity tools. However, it does require businesses to implement reasonable technical safeguards to protect customer information.

Technical safeguards help prevent unauthorized access, data theft, malware infections, and security breaches. Even small dealerships with limited budgets can significantly reduce risk by implementing basic security controls. The goal is to protect customer information wherever it is stored, transmitted, or accessed.

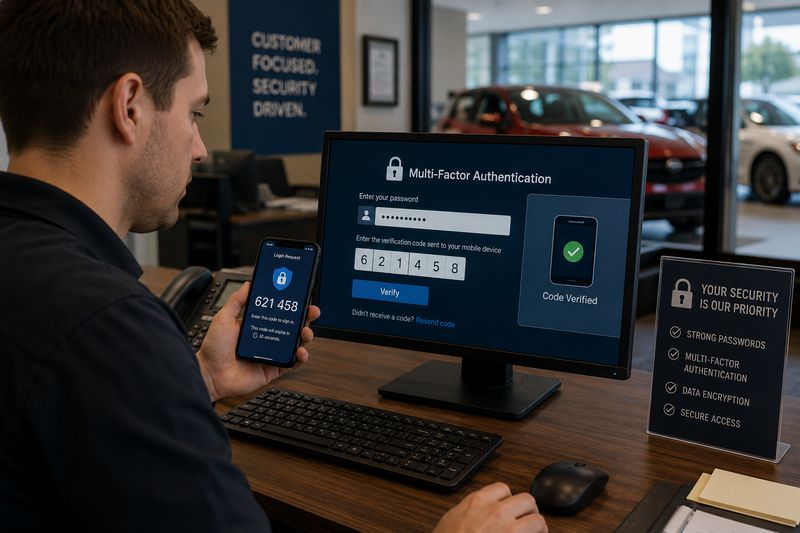

Multi-Factor Authentication (MFA)

Multi-factor authentication, commonly called MFA, is one of the most important security requirements under the Safeguards Rule.

MFA requires users to provide two or more forms of verification before accessing a system. This usually includes:

- a password;

- a code sent to a mobile device;

- an authentication application;

- a security key;

- biometric verification.

For example, a finance manager may enter a password and then receive a verification code on their phone before accessing customer credit applications.

Without MFA, a stolen password may give criminals immediate access to sensitive information. With MFA enabled, an attacker often cannot log in even if the password has been compromised.

MFA should be used whenever possible for:

- email accounts;

- dealer management systems;

- cloud storage;

- remote access;

- financial software;

- customer databases;

- vendor portals.

For many dealerships, enabling MFA is one of the fastest and most effective ways to improve security.

Data Encryption Requirements

Encryption protects information by converting it into unreadable data that can only be accessed with the proper authorization.

If encrypted data is stolen, it is often much more difficult for criminals to use.

Encryption may be used for:

- stored customer records;

- laptops and mobile devices;

- backup systems;

- cloud storage;

- emails containing sensitive information;

- data transferred between systems.

For example, if a dealership laptop containing customer records is stolen from an employee's vehicle, encryption may prevent unauthorized access to the information stored on the device.

Encryption is particularly important for:

- Social Security numbers;

- bank account information;

- credit applications;

- payment records;

- driver's license images.

Dealerships should work with their software providers and IT professionals to determine where encryption should be applied.

Secure Data Storage Practices

Customer information should be stored securely regardless of whether it exists in paper or electronic form.

Secure storage practices may include:

- password-protected systems;

- restricted access folders;

- encrypted storage devices;

- locked filing cabinets;

- secure cloud platforms;

- backup systems;

- access logs.

For example, scanned credit applications should not be saved on a shared desktop computer where every employee has access. Instead, they should be stored in protected systems that limit access to authorized personnel.

Dealerships should also review where information is stored. Customer records may exist in:

- dealer management software;

- CRM systems;

- email accounts;

- cloud drives;

- accounting systems;

- office computers;

- mobile devices.

Understanding where data is located is essential for protecting it.

Network Security Controls

The dealership network serves as the foundation for many business operations. Weak network security can expose multiple systems at the same time.

Network security controls may include:

- secure Wi-Fi networks;

- separate guest networks;

- access restrictions;

- network monitoring;

- secure routers;

- virtual private networks;

- administrative controls.

For example, customers using dealership Wi-Fi should not have access to internal business systems. A separate guest network can help reduce this risk.

Remote employees and outside vendors should also use secure connections when accessing dealership systems.

Strong network controls help prevent unauthorized access and reduce opportunities for attackers to move between systems.

Endpoint Protection and Antivirus Solutions

Endpoints are devices that connect to the dealership network. These include:

- desktop computers;

- laptops;

- tablets;

- smartphones;

- point-of-sale systems;

- office workstations.

Each endpoint can become an entry point for malware or cyberattacks.

Endpoint protection software helps detect and stop:

- viruses;

- ransomware;

- spyware;

- malicious downloads;

- suspicious activity.

For example, an employee may accidentally open a harmful email attachment. Antivirus and endpoint protection software may identify the threat before it spreads through the dealership network.

Modern endpoint protection often provides additional monitoring and alerts that help identify security problems quickly.

Small dealerships may not need advanced enterprise systems, but they should maintain updated protection on every device that stores or accesses customer information.

Firewalls and Intrusion Detection Systems

Firewalls help control traffic entering and leaving the dealership network. They act as a barrier between internal systems and outside threats.

A firewall may help:

- block unauthorized access;

- monitor network traffic;

- restrict suspicious activity;

- prevent certain attacks.

Intrusion detection systems monitor networks for unusual behavior and may alert administrators to possible attacks.

For example, if an unknown user attempts repeated login attempts against a dealership server, the system may generate an alert.

While large dealership groups may use advanced security monitoring tools, smaller dealers can still benefit from properly configured firewalls and managed security services.

These controls help reduce the risk of unauthorized access and improve overall network security.

Patch Management and Software Updates

Outdated software is one of the most common security weaknesses.

Cybercriminals often target known software vulnerabilities that have already been fixed by vendors. If dealerships delay updates, they may remain exposed to attacks.

Software that should be updated regularly includes:

- operating systems;

- dealer management software;

- accounting software;

- antivirus programs;

- web browsers;

- mobile applications;

- network equipment.

For example, an older office computer running unsupported software may create a security risk for the entire dealership.

Patch management means:

- identifying available updates;

- installing security patches;

- removing unsupported software;

- testing critical updates.

Regular updates help close known vulnerabilities before attackers can exploit them.

Secure Disposal of Customer Information

Customer information should not remain accessible after it is no longer needed. Improper disposal creates unnecessary risk.

Secure disposal methods may include:

- shredding paper documents;

- permanently deleting electronic files;

- wiping hard drives;

- destroying storage devices;

- securely erasing mobile devices;

- following retention policies.

For example, throwing old credit applications into a trash bin may expose customer information. Similarly, selling old computers without removing stored files may create serious security risks.

The dealership should establish clear retention and disposal procedures that explain:

- how long records are kept;

- who approves disposal;

- how records are destroyed;

- how destruction is documented.

Secure disposal is often overlooked, but it remains an important part of protecting customer information.

Access Controls and User Management

One of the simplest ways to protect customer information is to control who can access it. Many dealership data breaches happen not because of sophisticated hackers, but because too many employees have access to sensitive information.

The FTC Safeguards Rule expects dealerships to limit access to customer data and establish clear rules for managing user accounts. Every employee should only have access to the information necessary to perform their job.

Good access controls help reduce both internal mistakes and external threats.

Limiting Employee Access to Sensitive Data

Not every employee needs access to every customer record. Sales staff, finance managers, accounting personnel, service advisors, and managers often require different levels of access.

Sensitive information should only be available to employees who need it to perform their duties.

Examples include:

- Social Security numbers;

- credit reports;

- financing applications;

- bank account information;

- income verification documents;

- payment records;

- loan agreements.

For example, a salesperson may need access to customer contact information but may not need access to bank statements or credit reports. Likewise, a service advisor usually does not need access to financing documents.

Many smaller dealerships give all employees access to the same systems because it is easier to manage. However, broad access increases risk. If one account is compromised, more customer information may become exposed.

Limiting access reduces the potential damage from mistakes, stolen credentials, or unauthorized activity.

Role-Based Permissions

Role-based access means employees receive system permissions based on their job responsibilities.

Common dealership roles may include:

- sales staff;

- finance managers;

- accounting personnel;

- service employees;

- office managers;

- general managers;

- IT administrators.

Each role should have access only to the information required for that position.

For example:

- sales employees may access CRM records and customer contact information;

- finance personnel may access credit applications and loan documents;

- accounting staff may access payment information;

- management may review reports and security information.

This approach helps reduce unnecessary exposure to sensitive data.

Role-based permissions also make user management easier. When an employee changes positions, access rights can be updated without rebuilding the entire account structure.

For dealerships using dealer management systems, CRM software, or cloud applications, role-based permissions are often available through built-in settings.

Password Policies and Authentication Controls

Weak passwords remain one of the most common security problems in small businesses.

Examples of poor password practices include:

- shared passwords;

- simple passwords;

- passwords written on paper;

- passwords that never change;

- using the same password for multiple systems.

Dealerships should establish password policies that encourage stronger security.

Good password practices may include:

- unique passwords for each user;

- long and complex passwords;

- regular password updates when necessary;

- password managers;

- multi-factor authentication;

- account lockout settings.

For example, a shared login such as "Sales123" creates accountability problems because management cannot determine who accessed customer information.

Multi-factor authentication adds another layer of protection. Even if a password is stolen, an attacker may still be unable to access the account.

Authentication controls are particularly important for:

- email accounts;

- finance systems;

- dealer management software;

- cloud applications;

- remote access systems.

Monitoring User Activity

Monitoring user activity helps dealerships understand how customer information is accessed and used.

Activity monitoring may include:

- login records;

- access logs;

- failed login attempts;

- password changes;

- file downloads;

- administrative actions;

- unusual account behavior.

For example, if an employee account suddenly downloads hundreds of customer files after business hours, this activity may indicate a security problem.

Many modern software systems automatically record user actions. These records can help:

- identify unauthorized access;

- investigate incidents;

- support compliance efforts;

- improve accountability.

Monitoring does not mean constantly watching employees. Instead, it provides visibility into how systems are being used and helps identify unusual behavior.

For dealerships with limited IT resources, even basic logging and reporting can provide valuable information.

Managing Former Employee Access

One of the most common dealership security mistakes is leaving former employee accounts active after someone leaves the company.

Former employees may still have access to:

- email accounts;

- CRM systems;

- dealer management software;

- cloud storage;

- financing systems;

- remote access tools.

For example, a salesperson who left six months ago may still have access to customer records through an old login account. If those credentials are later stolen or misused, customer information could be exposed.

The dealership should establish procedures to:

- disable accounts immediately after termination;

- collect company devices;

- reset shared passwords;

- remove remote access privileges;

- revoke vendor access;

- document account removal.

Access reviews should also be conducted regularly to identify inactive accounts.

Removing unnecessary accounts is one of the simplest ways to reduce security risk.

Remote Access Security Requirements

Many dealerships now allow remote access for managers, accounting personnel, IT providers, or outside vendors. While remote access can improve productivity, it also creates additional security risks.

Remote access systems should include:

- multi-factor authentication;

- encrypted connections;

- secure passwords;

- limited user permissions;

- activity monitoring;

- access restrictions.

For example, an outside IT company may need temporary access to dealership systems for maintenance. That access should be limited, monitored, and removed when no longer needed.

Employees working from home should also follow security policies. Personal computers, unsecured Wi-Fi networks, and shared devices can create additional risks.

Dealerships should establish clear rules regarding:

- who may access systems remotely;

- which devices are allowed;

- how remote connections are secured;

- how activity is monitored.

The FTC Safeguards Rule does not prohibit remote access, but it expects dealerships to protect customer information regardless of where employees work.

Employee Training and Security Awareness

Employee training is one of the most important parts of FTC Safeguards Rule compliance. Even strong software and security tools can fail if employees do not understand how to protect customer information.

Auto dealerships are busy environments. Salespeople, finance managers, office staff, and managers handle customer data every day. A simple mistake, such as clicking a phishing link or emailing a credit application to the wrong person, can create serious risk. Training helps employees recognize these situations before they become expensive problems.

FTC Training Expectations

The FTC expects covered businesses to train employees on information security practices. Training should be connected to the dealership’s real risks, not just a generic online course that employees forget after completing it.

Employees should understand:

- what customer information must be protected;

- how to handle sensitive documents;

- how to recognize phishing emails;

- how to use passwords and MFA;

- how to report suspicious activity;

- who to contact when something goes wrong.

For example, a finance employee who works with credit applications needs more detailed training than a lot attendant who does not handle financing records. However, both employees should understand basic security rules, such as not sharing passwords and reporting suspicious emails.

Training should be practical, clear, and repeated over time.

Cybersecurity Awareness Programs

A cybersecurity awareness program teaches employees how to recognize everyday security risks. It should be simple enough for the whole team to understand and specific enough to match dealership operations.

A strong program may cover:

- password safety;

- email security;

- safe document handling;

- secure use of customer data;

- social engineering warning signs;

- safe internet use;

- device security;

- remote work rules;

- incident reporting.

For a small dealership, this program does not need to be expensive. It can include short training sessions, printed reminders, team meetings, and simple checklists.

For example, a dealership may hold a short monthly meeting to review one security topic, such as phishing emails or safe disposal of customer documents. Over time, these small sessions can build better habits across the team.

The goal is to make security part of daily work, not a one-time event.

Recognizing Phishing and Social Engineering Attacks

Phishing is one of the most common threats dealerships face. A phishing message may look like it comes from a lender, auction company, transport provider, software vendor, customer, or even dealership management.

Phishing emails may try to trick employees into:

- clicking a harmful link;

- opening a dangerous attachment;

- entering login credentials;

- sending customer documents;

- approving a fake payment;

- changing bank information.

Social engineering is similar, but it may happen by phone, text message, or in person. The attacker uses pressure, urgency, or trust to make an employee act quickly without checking.

Warning signs include:

- urgent payment requests;

- unexpected attachments;

- misspelled email addresses;

- unusual sender names;

- requests for passwords;

- links that do not match the sender;

- pressure to avoid normal approval steps.

For example, an employee may receive an email that appears to come from a lender asking for a customer’s Social Security number. Before sending anything, the employee should verify the request through a trusted contact method.

Employees should be trained to slow down, verify requests, and report anything suspicious.

Handling Customer Information Securely

Dealership employees should know how to handle customer information from the moment it is collected until it is securely stored or destroyed.

Secure handling practices include:

- collecting only necessary information;

- storing documents in approved locations;

- avoiding personal email for customer records;

- locking paper files when not in use;

- using approved systems for credit applications;

- avoiding shared passwords;

- not leaving customer documents on desks;

- shredding documents when no longer needed;

- sending sensitive information only through secure channels.

For example, a salesperson should not take a photo of a customer’s driver’s license on a personal phone unless the dealership has a secure approved process for that. A finance manager should not leave credit applications sitting on a printer overnight.

These small habits matter because many data exposures happen through ordinary daily mistakes.

Clear rules help employees understand what is allowed and what is not.

Ongoing Employee Education

Security training should not happen only when an employee is hired. Cyber threats change, dealership software changes, and employees may forget rules over time.

Ongoing education may include:

- annual training;

- new-hire training;

- short monthly security reminders;

- phishing simulations;

- updates after policy changes;

- refresher training after incidents;

- role-specific training for finance or management staff.

For example, if the dealership starts using a new online credit application system, employees should receive training on how to use it securely. If a phishing attempt targets the dealership, management can use it as a learning opportunity for the whole team.

Ongoing training helps create a culture where employees feel responsible for protecting customer information.

It also helps reduce careless habits, such as sharing passwords or storing files in the wrong place.

Documenting Training Activities

Training must be documented. If a dealership cannot show that training happened, it may be difficult to prove that employees were properly educated.

Training records may include:

- training dates;

- topics covered;

- employee attendance;

- course completion records;

- signed acknowledgments;

- training materials;

- quiz results;

- refresher training notes.

For example, after a short training session on phishing emails, the dealership should record who attended, what was covered, and when the session took place.

Documentation does not need to be complicated. A simple spreadsheet, signed form, or digital training report can be enough for many small dealerships.

Good records help show that the dealership takes security seriously and is working to meet FTC Safeguards Rule expectations.

Make Better Inventory Decisions with Auction Data

Strong dealership operations depend on both data security and smart inventory purchasing. BidNDrive provides access to vehicle history reports, sold auction prices, and market information that help dealers reduce financial risks before buying vehicles.

- ✅ Free auction history reports

- ✅ Sold vehicle price information

- ✅ Access to nationwide inventory

- ✅ No fees for unsuccessful bids

Managing Third-Party Vendors and Service Providers

Auto dealerships rarely handle customer information alone. Most dealers work with lenders, software providers, payment processors, CRM platforms, marketing tools, cloud storage systems, IT companies, transport partners, and other service providers.

The FTC Safeguards Rule expects dealerships to pay attention to vendor security because third parties may have access to sensitive customer information. If a vendor handles dealership data poorly, the dealership may still face business, legal, and reputation risks.

Why Vendor Security Matters

Vendor security matters because customer information often moves outside the dealership’s direct control. A dealer may protect its own computers, but still expose customer data through a weak vendor system.

Vendors may access or store:

- credit applications;

- customer contact details;

- driver’s license copies;

- financing documents;

- payment information;

- CRM records;

- deal jackets;

- email communications;

- cloud files.

For example, a small used car dealer may use an outside CRM platform to manage leads and customer records. If that CRM account is not properly secured, customer information could be exposed even if the dealership’s office computers are protected.

A vendor breach can create problems such as:

- customer data exposure;

- business interruption;

- regulatory questions;

- legal expenses;

- loss of customer trust;

- expensive system recovery.

Dealerships should treat vendor security as part of their own information security program.

Evaluating Vendor Cybersecurity Practices

Before working with a vendor that handles customer information, dealerships should evaluate how that vendor protects data.

This does not always require a complex audit. For many small dealerships, the first step is asking practical questions and reviewing available security documentation.

Important questions include:

- What customer information will the vendor access?

- Where will the data be stored?

- Is the data encrypted?

- Does the vendor use multi-factor authentication?

- Who can access dealership data?

- How does the vendor train its employees?

- Does the vendor have an incident response plan?

- How quickly will the vendor notify the dealership after a breach?

- Does the vendor use subcontractors?

- How is data deleted when the contract ends?

For example, if a dealership uses a cloud-based document storage provider, it should understand whether files are encrypted, who can access them, and how accounts are protected.

The level of review should match the risk. A vendor that only prints business cards is different from a vendor that stores credit applications or Social Security numbers.

Required Contractual Safeguards

Vendor contracts should include security requirements when the vendor handles customer information. Verbal promises are not enough.

A good vendor agreement may address:

- protection of customer information;

- limits on data use;

- confidentiality obligations;

- access controls;

- encryption requirements;

- breach notification duties;

- subcontractor controls;

- secure data return or deletion;

- compliance with applicable laws;

- audit or review rights.

For example, a dealership using a third-party finance platform should have a contract stating that the vendor must protect customer financial data and notify the dealership if a security incident occurs.

These contract terms help clarify expectations before a problem happens.

Small dealerships may not have in-house legal teams, so vendor contracts should be reviewed carefully before signing. If a vendor refuses to explain its security practices or include basic data protection terms, that may be a warning sign.

Monitoring Service Provider Compliance

Vendor management does not stop after signing a contract. Dealerships should monitor vendors over time, especially those with access to sensitive customer information.

Ongoing monitoring may include:

- reviewing vendor security updates;

- confirming MFA and access controls;

- checking breach notifications;

- reviewing contract renewals;

- confirming data retention practices;

- removing vendors that are no longer needed;

- reviewing user access inside vendor systems.

For example, a dealership may stop using a marketing platform but forget that the platform still contains old customer lists. If the account remains active and unsecured, customer data may still be at risk.

Dealerships should maintain a vendor list that includes:

- vendor name;

- service provided;

- type of customer data accessed;

- contract status;

- security review date;

- responsible dealership contact.

This makes it easier to track which third parties may affect customer information.

Cloud Storage and Software Provider Risks

Cloud tools can help dealerships work faster and reduce paper storage, but they also create security risks if not managed properly.

Common cloud and software risks include:

- weak passwords;

- no multi-factor authentication;

- shared employee accounts;

- excessive user permissions;

- public file-sharing links;

- poor vendor security;

- unclear data retention rules;

- former employees with access;

- unsupported software.

For example, a dealership may store scanned credit applications in a shared cloud folder. If the folder is accidentally set to public access, sensitive information could be exposed.

Cloud systems should be configured carefully. Dealerships should use strong passwords, MFA, role-based permissions, and regular access reviews.

Software providers should also be reviewed. Dealer management systems, CRM tools, payment platforms, and online credit application providers may store some of the dealership’s most sensitive data.

The safest approach is to know exactly where customer information is stored and who can access it.

Vendor Breach Response Expectations

Dealerships should know what happens if a vendor experiences a data breach. Waiting until after an incident can cause confusion and delays.

A vendor breach response plan should answer:

- How will the vendor notify the dealership?

- How quickly will notice be provided?

- What information will the vendor share?

- Who at the dealership will respond?

- Will customers need to be notified?

- Will legal or regulatory reporting be required?

- How will affected systems be secured?

- What steps will prevent a similar issue?

For example, if a financing software provider reports unauthorized access, the dealership must quickly determine what customer information was affected and what actions are required.

The dealership should not assume the vendor will handle everything. Even when the incident starts with a third party, the dealership may still need to communicate with customers, regulators, lenders, or legal advisors.

Developing an Incident Response Plan

No dealership can completely eliminate the risk of a cybersecurity incident. Even businesses with strong security controls may experience phishing attacks, malware infections, vendor breaches, or unauthorized access attempts.

The FTC Safeguards Rule requires covered businesses to develop an incident response plan. This plan helps dealerships respond quickly, reduce damage, protect customer information, and restore operations after a security event. For many dealerships, having a plan before an incident occurs can save both money and valuable time.

What Is an Incident Response Plan?

An incident response plan is a written document that explains what the dealership should do if a security incident occurs.

A security incident may include:

- ransomware attacks;

- phishing attacks;

- stolen laptops;

- unauthorized account access;

- malware infections;

- lost customer records;

- vendor breaches;

- stolen passwords;

- data leaks;

- system failures affecting customer information.

The purpose of the plan is to avoid confusion during an emergency. Employees should know who to contact, what actions to take, and how to protect customer information.